Getting a denial letter after a roof damage claim feels like a gut punch, especially when you’ve paid your premiums faithfully for years. Understanding why insurance denies roof claims is the first step to protecting yourself, because many of these denials are not final and several are based on gaps you can actually address. This guide breaks down the exact reasons insurers reject roof claims, the policy language they rely on, and the practical steps you can take to push back effectively.

Table of Contents

- Common reasons insurers deny roof claims

- How roof age and cosmetic damage affect claim decisions

- Policy clauses and legal rules that influence claim outcomes

- Steps to take when your roof insurance claim is denied

- Documentation and maintenance: the key to successful claims

- Why many roof insurance claim denials are avoidable misconceptions

- How Vector Claim Solutions helps denied roof insurance claims

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

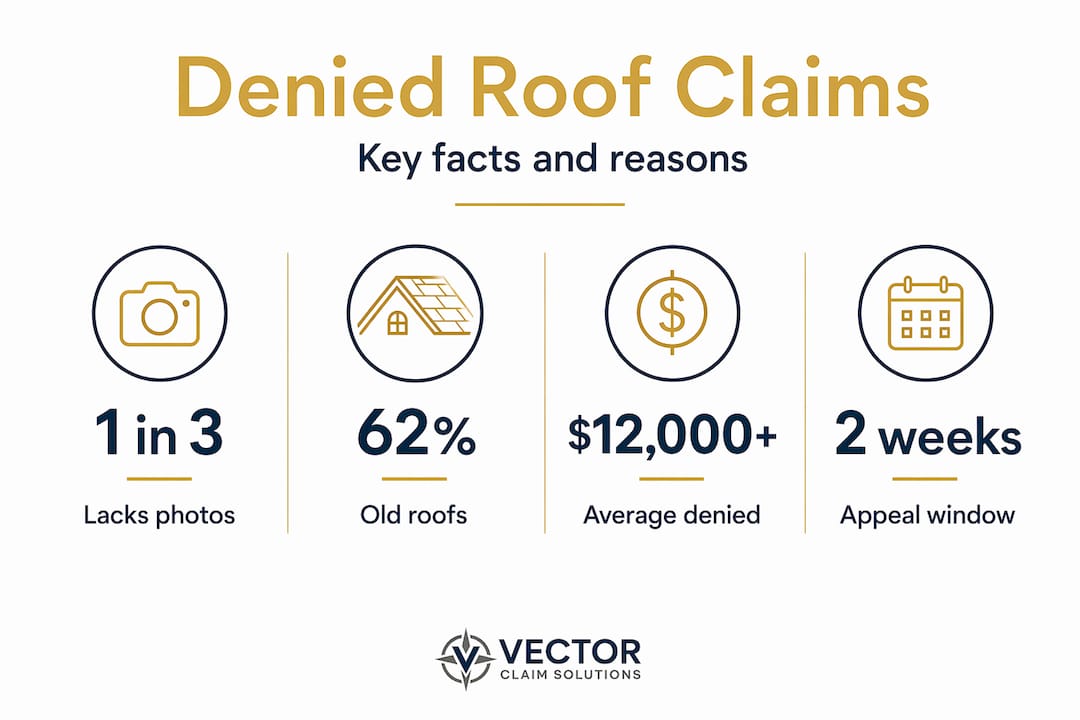

| Documentation matters | Over one-third of denied claims are due to insufficient photos and evidence of roof damage. |

| Roof age limits coverage | Roofs over 10 years old often face claim denials or reduced payments for wear-related damage. |

| Policy exclusions are common | Wear and tear, lack of maintenance, and cosmetic damage are standard reasons insurers deny claims. |

| Know your rights | State laws require insurers to promptly acknowledge and decide claims with penalties for violations. |

| Appeal actively | Successful appeals depend on contractor reports, re-inspections, and formal complaints to insurance departments. |

Common reasons insurers deny roof claims

Insurance companies don’t deny claims arbitrarily. They follow policy language carefully, and the denial reasons they cite usually fall into a handful of predictable categories. Knowing these categories in advance changes how you document damage, file your claim, and respond when things go wrong.

The most frequent roof claim denial reasons include:

- Wear and tear or aging: Standard HO-3 policies explicitly exclude wear and tear, gradual deterioration, and lack of maintenance. If an insurer can argue your roof deteriorated over time rather than through a sudden event, they will.

- Insufficient documentation: A 2023 TDI case study found that 37% of denied claims were rejected due to insufficient photographic proof of damage. No photos, no proof.

- Cosmetic damage exclusions: Surface dents or scuffs that don’t affect the roof’s function are often excluded, particularly with endorsements added to policies in hail-prone states like Texas and Colorado.

- Late reporting: Many policies require you to report damage “promptly” after a storm. Waiting weeks or months gives insurers grounds to deny based on late notification.

- Pre-existing damage: If the insurer’s adjuster finds damage that predates your claim event, they can deny coverage for the entire claim or reduce payment significantly.

- Wrong coverage type: Some homeowners assume their policy covers all damage. Flood damage to a roof, for example, requires a separate flood policy.

“The insurer’s job is to pay what the policy requires, not what you expect. The homeowner’s job is to understand the difference before filing.”

Most policyholders who accept a denial at face value don’t realize the denial often rests on a single disputed point, such as whether damage was sudden or gradual. That’s a question that can be answered with the right inspection report and documentation.

Pro Tip: If your denial letter is vague about which policy exclusion applies, call your insurer and request a written explanation citing the specific policy language. Vague denials are easier to challenge than detailed ones.

If you are already dealing with a denied claim, exploring your roof damage claims support options early can prevent missed deadlines that would close off your appeal rights.

How roof age and cosmetic damage affect claim decisions

Roof age is one of the most consequential factors affecting roof claims, and it surprises many homeowners. Insurers frequently implement “10-year roof rules” or cosmetic damage exclusions that allow them to deny claims for roofs older than 10 years or for damage deemed purely aesthetic.

Here is how these two factors typically play out in real claims:

| Factor | How insurer treats it | Likely outcome for homeowner |

|---|---|---|

| Roof under 10 years old | Generally covered at replacement cost value (RCV) | Full replacement cost if damage confirmed |

| Roof 10 to 20 years old | Often covered at actual cash value (ACV) | Depreciation applied, lower payout |

| Roof over 20 years old | May be denied or covered at minimal ACV | Partial payment or outright denial |

| Cosmetic damage only | Excluded by endorsement in many states | Denial with no compensation |

| Functional damage (leaks, structural issues) | Covered regardless of roof age in most cases | Claim typically approved |

What “actual cash value” really means for you: ACV is the replacement cost minus depreciation. On a 15-year-old roof with a 20-year expected lifespan, the insurer might calculate depreciation at 75%, leaving you responsible for a large portion of the replacement cost out of pocket.

Understanding cosmetic versus functional damage is equally important. A hail storm that leaves small dents in metal flashing but does not compromise the roof’s ability to shed water may be classified as cosmetic. However, if granule loss from those same hailstones accelerates shingle wear and reduces the roof’s protective lifespan, that can qualify as functional damage, which most policies do cover.

- Ask your contractor to document why the damage is functional, not just that damage exists

- Reference manufacturer specifications where relevant, because some manufacturers void warranties after hail impact regardless of visible damage

- Request that your adjuster note specific findings per roof section, not just a general assessment

Pro Tip: Before filing your claim, read your policy’s declarations page and any endorsements carefully. Look for terms like “cosmetic damage exclusion” or “ACV roof settlement.” These tell you exactly what coverage you’re working with before you invest time in a claim fight.

For a deeper look at whether your situation calls for a repair or full replacement, the roof repair vs replacement insurance guide walks through the coverage distinctions in plain language.

Policy clauses and legal rules that influence claim outcomes

Two policy clauses catch homeowners off guard more than any others: the Anti-Concurrent Causation clause and maintenance exclusions. Understanding both can dramatically change how you approach documentation and appeals.

The four most important policy and legal factors to know:

-

Anti-Concurrent Causation (ACC) clause: This clause allows insurers to deny claims when damage results partly from an excluded cause, such as existing wear, even if a covered event like hail also contributed. The burden falls on you to separate the storm damage from the pre-existing condition. This is where a detailed contractor inspection becomes critical.

-

Maintenance exclusions: Policies won’t cover damage that results from neglect or deferred maintenance. If your gutters were clogged and water backed up under shingles, that’s maintenance neglect, not storm damage. Keep records of any maintenance work performed on your roof.

-

State-mandated insurer timelines: Texas Department of Insurance guidelines mandate that insurers acknowledge claims within 15 days and make a coverage decision within 15 business days after receiving all requested information. Nebraska, Iowa, Colorado, and Florida each have comparable regulations. If your insurer misses these deadlines, document it and cite it in any appeal or complaint.

-

Prompt reporting requirements: Filing your claim quickly after a storm matters. Most policies require timely notification. If you delay reporting, the insurer has grounds to argue they were unable to assess the original damage, which can result in a denial.

“An insurer that drags its feet past state-mandated deadlines has already given you grounds for a stronger appeal. Don’t overlook that leverage.”

Understanding these policy mechanics helps you see claims not as a favor the insurer grants, but as a contract obligation they must meet under specific conditions. Learning how your state’s rules apply is a meaningful part of navigating a property insurance claim successfully.

Steps to take when your roof insurance claim is denied

A denial is not the end of the road. Most homeowners never challenge a denial, which is exactly what insurers count on. Here is a structured approach to appealing effectively.

-

Request a detailed written denial letter. Ask the insurer to cite the specific policy language and section numbers that justify the denial. Vague denials are legally weaker and easier to contest.

-

Hire a licensed contractor for an independent inspection. Make sure the report directly addresses the insurer’s stated denial reasons. A generic inspection report won’t move the needle. You need a document that counters the insurer’s specific arguments.

-

Gather timestamped photographic and video evidence. Capture every area of damage clearly before any work begins. Successful appeals consistently involve detailed inspection reports, re-inspection requests, timestamped photos, and formal complaints to state regulators.

-

Request a re-inspection by a different adjuster. You have the right to ask for a second look. If the original adjuster missed covered damage or misclassified it, a different set of eyes can change the outcome.

-

File a formal complaint with your state insurance department. In Texas, that’s the Texas Department of Insurance. In Nebraska and Iowa, it’s their respective insurance divisions. Filing a complaint creates a formal record and often prompts insurers to reconsider their position.

-

Consider legal or professional representation. If all else fails, a public adjuster or attorney specializing in insurance claims can evaluate your case and take formal action on your behalf.

Pro Tip: Keep every communication with your insurer in writing. Phone calls are easy to dispute. Emails and written letters create a paper trail that supports your appeal and any future complaint.

Reviewing the process of appealing a property insurance claim and using a hail damage inspection checklist are two practical steps you can take today to build a stronger case.

Documentation and maintenance: the key to successful claims

The single biggest controllable factor in any roof insurance claim is documentation quality. Nearly 37% of denied claims were rejected simply because homeowners lacked sufficient photographic proof of damage. That statistic represents thousands of preventable denials.

What proper documentation looks like:

- High-resolution photos and video of every damaged area, taken immediately after the storm event

- Date and time stamps on all images, either through your phone’s automatic metadata or a handwritten log

- Labeled photos showing context, such as the roof section, compass direction, and visible damage type

- A written timeline noting when the storm occurred, when you discovered damage, and when you filed your claim

- Copies of all maintenance records, contractor invoices, and prior inspection reports

One homeowner in the Dallas area saw an initial $12,000 roof claim denied based on an insurer claim of pre-existing wear. By presenting dated photos from a contractor inspection done six months before the storm, along with photos taken the morning after the hail event, they were able to demonstrate the damage was clearly new. The claim was reversed and paid in full.

Avoid one critical mistake: Do not start repairs before your insurer’s adjuster has completed their inspection. Insurers regularly deny claims when evidence has been altered or removed, because they cannot verify the original scope of damage.

Pro Tip: Set up a simple folder on your phone or computer labeled with your address and date, and drop storm damage photos in it immediately. If you ever need them for a claim, they’ll be organized and timestamped without any extra effort.

Pairing good documentation habits with a thorough storm damage claim checklist gives you the clearest possible picture of what happened and when, which is exactly what insurers need before approving payment.

Why many roof insurance claim denials are avoidable misconceptions

After working through hundreds of roof claims across Texas, Nebraska, Colorado, Iowa, and Florida, we see the same patterns repeat. The most fundamental one: homeowners treat their insurance policy like a maintenance plan.

The most common misconception is that homeowners insurance covers any roof problem, when in fact insurers are designed to cover sudden, accidental events, not the natural aging of building materials. When a hailstorm hits a 15-year-old roof, the insurer’s instinct is to look for evidence that the damage was really just the aging process accelerating. That framing benefits them.

What we find just as frustrating is how limited inspections often overlook hidden damage, and how vague denial letters leave homeowners confused about their actual rights. A denial letter that says “damage due to wear and tear” without citing a specific policy section is not a complete answer. It’s a starting point for your response.

The homeowners who recover their claims are not the ones who got lucky. They are the ones who asked for specifics, got independent inspections, and refused to treat a denial letter as the final word. Understanding roof claim negotiation dynamics gives you a realistic picture of what’s actually happening behind the scenes when your claim is evaluated.

The uncomfortable truth is that the insurance claim process rewards preparation and persistence. It does not reward passivity. If you document your damage well, understand your policy exclusions, and know your state’s rules, you are in a far stronger position than the insurer expects you to be.

How Vector Claim Solutions helps denied roof insurance claims

Facing a denied or underpaid roof claim on your own is stressful, and one misstep can close off your options. We work directly on your behalf as licensed public adjusters, reviewing your claim from the ground up to identify where coverage was wrongly denied, how documentation gaps can be addressed, and what insurance companies actually factor into claim payments before they issue a settlement.

Our team specializes in storm, hail, and wind damage claims across Nebraska, Iowa, Colorado, Texas, and Florida, the same states where these claim disputes are most common. If you’ve received a denial or a settlement that doesn’t cover your actual repair costs, a free claim review and second opinion can clarify your position before you decide on next steps. Whether you need documentation support, negotiation help, or someone to represent you through a formal appeal, working with a public adjuster ensures you have an experienced advocate in your corner. Reach out before your appeal deadline closes.

Frequently asked questions

Why did my insurance company deny my roof damage claim?

Many claims are rejected due to missed deadlines, insufficient proof, or damage attributed to normal wear and tear. Policy exclusions for cosmetic damage and lack of maintenance are also common denial reasons.

Can I appeal my denied roof insurance claim?

Yes. Successful appeals involve detailed independent inspection reports, a written demand for specific policy citations, re-inspection requests, and formal complaints to your state insurance department.

Does roof age affect insurance claim approvals?

Yes. Insurers apply “10-year roof rules” that allow them to deny claims or settle at actual cash value for older roofs, significantly reducing what you receive compared to a newer roof.

What documentation do I need to avoid claim denials?

You need timestamped high-resolution photos taken before any repairs, maintenance and inspection records, and a licensed contractor’s report that directly addresses the insurer’s denial reasons. Insufficient photographic proof accounts for over a third of all denied claims.

What happens if I start repairs before the insurance adjuster inspects the roof?

Insurers can deny claims when repairs begin before their inspection because they can no longer verify the original scope of damage. Document everything thoroughly and delay repairs until after inspection whenever possible.