When you file a property insurance claim, you probably expect a straightforward process: damage happens, you report it, and your insurer pays to fix it. The reality is far more complicated. Claim payouts are calculated through a layered process involving coverage determinations, valuation methods, depreciation schedules, and deductibles, and each step can reduce what you receive. Understanding how these calculations work is the most direct path to a fair settlement, whether you own a single-family home in Nebraska or a commercial building in Texas.

Table of Contents

- How insurers calculate your claim: the standard process

- The key factors that impact your payout

- ACV vs RCV: why valuation methods matter

- Special rules for commercial property claims: the coinsurance penalty

- What state laws require for insurance claim payments

- A veteran claim expert’s take: don’t let hidden rules shortchange your claim

- Get expert help maximizing your claim payout

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Valuation method matters | Whether your policy is ACV or RCV can greatly affect the amount you receive. |

| Deductibles reduce payouts | All claim payments are lowered by your deductible, which comes out of your pocket. |

| Documentation is crucial | Submitting clear repair receipts can unlock additional payments under RCV policies. |

| Commercial policies face coinsurance | Underinsuring commercial property can result in harsh penalty formulas that decrease your payout. |

| Timelines are set by state laws | Most states require insurers to settle valid claims within 30–60 days after documentation is delivered. |

How insurers calculate your claim: the standard process

Now that you know why clarity is essential, let’s see how your insurer actually arrives at a payment amount. The process is more structured than most policyholders realize, and each stage creates an opportunity for the outcome to shift in your favor or against it.

According to standard industry practice, insurers inspect damage, determine coverage, and calculate payouts based on your specific policy terms and limits. Here is how that typically unfolds:

- Initial inspection. A company adjuster visits your property to document visible damage. The quality and thoroughness of this inspection directly affects your payout. Adjusters working high-volume storm events often move quickly, and missed damage at this stage can mean missed dollars later.

- Coverage determination. The adjuster reviews your policy to confirm which damages are covered perils. A wind event, for example, may cover roof damage but not pre-existing deterioration. This distinction matters enormously.

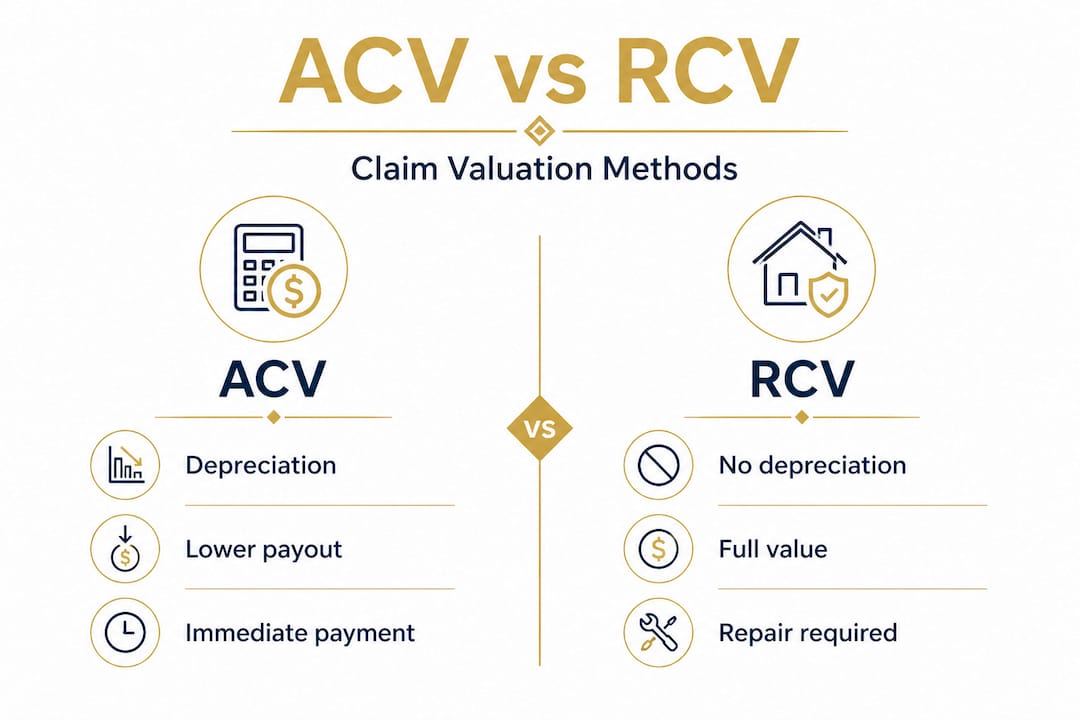

- Valuation of the loss. The insurer assigns a dollar value to each damaged item or system using either actual cash value (ACV) or replacement cost value (RCV), which we will explain in detail shortly.

- Deductible application. Your deductible is subtracted from the calculated loss amount. This is non-negotiable under your policy terms.

- Final payout issued. The net amount after deductibles and any depreciation withheld is sent to you, often with a detailed explanation of benefits.

Important: Your documentation matters just as much as the adjuster’s. Repair receipts and documented evidence can determine whether recoverable depreciation gets released back to you after repairs are completed. Never discard invoices, contractor estimates, or photos.

Understanding the insurance claim process explained in full can help you avoid common missteps that lead to underpayment. For additional guidance, you can also find more claim insights covering a wide range of property loss scenarios.

The key factors that impact your payout

Having traced the claim calculation process, it’s vital to understand which specific factors insurers consider when setting your payout. These are the variables that most directly determine whether your settlement covers your actual repair costs or leaves you short.

Valuation method: ACV vs. RCV

This is the single biggest factor. ACV incorporates depreciation while RCV pays replacement cost without a depreciation deduction. On a 15-year-old roof, the difference between these two methods could easily be $8,000 to $15,000 on a mid-sized home. If your policy uses ACV, you absorb that depreciation gap out of pocket.

Deductibles

Settlements equal the covered loss minus your deductible, always. A $2,500 wind/hail deductible on a $10,000 roof claim leaves you with $7,500 before any depreciation. Some states allow percentage-based deductibles, which can be significantly higher on larger homes.

Depreciation schedules

Even under RCV policies, insurers withhold depreciation initially and release it only after you document completed repairs. The older your property components, the more depreciation is withheld. A 20-year-old HVAC system may carry heavy depreciation that reduces your initial check substantially.

Scope disagreements

Insurers may limit the scope of repairs to what their adjuster documented. If the adjuster missed damaged gutters, interior water intrusion, or soft-metal damage from hail, those items simply won’t appear in the estimate. This is one of the most common reasons policyholders receive less than they deserve.

Here is a summary of key factors at a glance:

- Policy type (ACV vs. RCV): Determines whether depreciation is withheld

- Deductible amount: Directly reduces your final check

- Age and condition of property: Affects depreciation calculations

- Quality of damage documentation: Influences what gets included in the scope

- Roof age endorsements: Some policies now limit roof coverage based on age

- Coverage limits: Caps the maximum payout regardless of actual damage

Pro Tip: Review your policy’s declarations page before a storm season. Knowing your deductible type, coverage limits, and valuation method lets you plan financially and respond faster after a loss.

Understanding how deductibles and reduced payouts interact with your settlement can help you spot when an estimate looks too low. For roofing claims specifically, the roof claim calculation process has its own set of rules that affect whether you receive a repair or full replacement.

ACV vs RCV: why valuation methods matter

With the major factors in mind, let’s break down how valuation types actually change what you’re paid. This is where many policyholders are caught off guard, especially after a major storm.

| Feature | ACV (Actual Cash Value) | RCV (Replacement Cost Value) |

|---|---|---|

| Depreciation applied | Yes, reduces your payout | Withheld initially, then released |

| Initial payment | Depreciated value only | Depreciated value (ACV portion) |

| Second payment | None | Released after documented repairs |

| Out-of-pocket risk | Higher | Lower, if repairs are documented |

| Best for | Older properties or lower premiums | Newer properties or full coverage |

A real-world example

Say your 12-year-old roof is destroyed by hail. The replacement cost is $18,000. The insurer calculates 40% depreciation based on the roof’s age and condition, bringing the ACV to $10,800. Your deductible is $1,500.

Under an ACV policy, you receive $10,800 minus $1,500, which equals $9,300. You cover the remaining $8,700 yourself.

Under an RCV policy, here is how the payment typically flows:

- Initial payment: $10,800 (ACV) minus $1,500 deductible equals $9,300.

- You complete repairs and submit documentation to your insurer.

- Second payment: The withheld depreciation of $7,200 is released to you.

- Total received: $16,500 out of the $18,000 replacement cost, with $1,500 covered by your deductible.

RCV policies pay an initial ACV amount, then release the recoverable depreciation after you document completed repairs. This two-payment structure catches many homeowners off guard. They receive the first check, assume the claim is closed, and never follow up to collect the second payment.

To protect yourself, always ask your insurer whether your claim has remaining recoverable depreciation and what documentation is needed to release it. Learn more about the full RCV payment process and what it means for your residential claim.

Special rules for commercial property claims: the coinsurance penalty

We’ve covered homeowner policies. Now let’s address a crucial but often misunderstood rule that impacts commercial claims. If you own a commercial building, this section could save you tens of thousands of dollars.

If your insured limit falls below a required percentage of replacement value, your insurer can apply a penalty formula that reduces your payout, even on a valid claim. This is the coinsurance clause, and it operates silently in the background until you file a claim.

How the coinsurance formula works

Most commercial policies require you to insure your property to at least 80% of its replacement value. If you fall short, the insurer applies this formula:

(Amount of insurance carried / Amount required) x Loss amount = Payout

| Building Value | Required Coverage (80%) | Actual Coverage | Coinsurance Penalty | $200,000 Loss Payout |

|---|---|---|---|---|

| $1,000,000 | $800,000 | $800,000 | None | $200,000 |

| $1,000,000 | $800,000 | $600,000 | Yes | $150,000 |

| $1,000,000 | $800,000 | $400,000 | Yes | $100,000 |

As the table shows, being underinsured by 25% on a $200,000 loss costs you $50,000 out of pocket. That is a significant financial hit that most business owners never anticipate.

Here is what commercial property owners should watch for:

- Annual policy reviews: Building values change. If you haven’t updated your coverage limits in three or more years, you may be underinsured without knowing it.

- Renovation and improvements: Any significant upgrades increase your replacement value and should trigger a coverage review.

- Agreed value endorsements: Some policies offer this option to eliminate the coinsurance penalty entirely.

- Inflation guard provisions: These automatically adjust your coverage limits to keep pace with construction cost increases.

Pro Tip: Ask your commercial insurance agent to provide a replacement cost estimate for your building every two to three years. The cost of a proper appraisal is minor compared to the risk of a coinsurance penalty during a large loss.

For a deeper look at how this affects your business, review our commercial coinsurance explained overview or explore how we review commercial claims for underpayment and improper scope.

What state laws require for insurance claim payments

Once your payout is calculated, when can you expect the insurer to actually send the money? That’s where state laws come in. Most policyholders don’t realize they have legal protections around payment timing, and knowing these rights can help you push back if your insurer drags its feet.

State rules commonly require prompt settlement practices, with many states mandating payment of valid claims within specific timeframes after documentation is received. While exact deadlines vary by state, the general framework looks like this:

- Acknowledgment of claim: Typically required within 10 to 15 days of filing

- Coverage decision: Insurers usually must accept or deny within 15 to 30 days of receiving all documentation

- Payment issuance: Most states require payment within 30 to 60 days after a valid proof of loss is submitted

- Interest on delayed payments: Some states require insurers to pay interest if they miss payment deadlines

In states like Texas and Florida, where storm claims are frequent and high-volume, these rules carry real weight. Texas law, for example, requires insurers to pay within five business days of approving a claim. Florida has its own prompt payment statutes with specific penalties for non-compliance.

Know your rights: If your insurer is slow to respond after you’ve submitted complete documentation, you may have grounds to file a complaint with your state’s department of insurance. Documenting every communication, including dates and the names of representatives you speak with, strengthens your position significantly.

The key takeaway is this: submit your documentation as completely and quickly as possible. Every delay on your end resets the clock on the insurer’s obligations. Keep copies of everything you send, use certified mail when submitting formal documents, and follow up in writing.

A veteran claim expert’s take: don’t let hidden rules shortchange your claim

Here is something most guides won’t tell you. The regulations and timelines described above represent the minimum standard. Real-world claims, especially after major storms across Nebraska, Iowa, Colorado, Texas, and Florida, are decided by details that go far beyond the basics.

Over the years, we’ve seen policy language shift in ways that quietly reduce coverage without policyholders ever noticing. One of the most significant recent changes is the introduction of ACV-only endorsements for roofs. These endorsements, sometimes buried in renewal documents, convert your roof coverage from RCV to ACV regardless of what the rest of your policy says. A homeowner with a 10-year-old roof and an ACV endorsement may receive $4,000 less than their neighbor with identical damage and an RCV policy.

We’ve also seen insurers make honest mistakes. An adjuster who visits a property after a hailstorm may document visible shingle damage but miss hail strikes on gutters, downspouts, window screens, HVAC equipment, and painted surfaces. Each of those missed items has a dollar value. Collectively, they can represent 20% to 40% of the true claim value. Your documentation, your photos, your contractor’s assessment, these are not just supporting materials. They are often the deciding factor in whether those items get included.

Persistence matters too. Insurers sometimes issue a first payment and consider the matter resolved. If you accept that check without reviewing the scope carefully, you may be closing the door on legitimate additional coverage. We consistently find that policyholders who request a claim review after receiving a settlement often recover meaningful additional funds, not because the insurer acted in bad faith, but because the initial scope was incomplete.

The most important thing you can do is treat your claim as an active process, not a passive one. Engage with the documentation, ask questions, and don’t hesitate to bring in professional help when the numbers don’t add up.

Get expert help maximizing your claim payout

If you’re feeling overwhelmed by the rules and calculations, professional help can make all the difference. Navigating depreciation schedules, coinsurance formulas, and state-specific timelines is genuinely complex, and the stakes are high.

At Vector Claim Solutions, we work exclusively on behalf of policyholders, never insurance companies. We review what was damaged, what your policy actually covers, and what it takes to restore your property correctly. Whether you need help understanding how to navigate claims from the start or you’ve already received a settlement that feels too low, we can help. Request a personalized insurance claim review today, or explore the full range of claim types handled to see how we can support your specific situation.

Frequently asked questions

How do insurers decide between ACV and RCV for claim payouts?

They use the policy wording: ACV incorporates depreciation while RCV pays replacement cost without a depreciation deduction, typically requiring receipts for completed repairs before releasing the full amount.

Does every homeowner receive full replacement cost under RCV policies?

No. Insurers pay the depreciated ACV amount first, then require proof of completed repairs before releasing the remaining recoverable depreciation as a second payment.

How does my deductible affect the insurance payment I receive?

Your settlement is reduced by your deductible amount every time, which you pay out of pocket before any insurance funds are applied to your loss.

What is the coinsurance penalty and who does it impact?

It impacts commercial property owners who underinsure their buildings. If coverage falls below the required percentage of replacement value, a penalty formula reduces your payout even on a fully valid claim.

How long do insurers have to pay my claim after approval?

Most states require payment within 30 to 60 days of receiving all necessary documentation, though some states like Texas have even tighter deadlines for approved claims.