Most property owners think getting documentation together after a storm means gathering photos and waiting. The reality is quite different. Understanding how public adjuster documents are structured is what separates a claim that settles quickly and fairly from one that drags on, gets underpaid, or gets denied outright. This guide walks you through the purpose, components, and layout of public adjuster documentation so you know exactly what a credible claim file looks like and why every piece of it matters.

Table of Contents

- The core purpose of public adjuster documentation and what it includes

- How a typical public adjuster file is organized: chronology, evidence, and estimate details

- Common documentation pitfalls and how to avoid them

- Practical steps for property owners: assembling and managing your documentation effectively

- How different states’ conditions affect public adjuster documentation needs

- Why the conventional paperwork mindset misses the real power of public adjuster documentation

- How Vector Claim Solutions supports your claim through expert documentation and negotiation

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Documentation creates success | A clear, chronological, and auditable evidence chain is essential for a credible insurance claim. |

| Photos with metadata | Timestamped and GPS-tagged photos vastly improve the trustworthiness of your claim evidence. |

| Avoid gaps | Continuous daily reports before, during, and after an event prevent credibility issues and delays. |

| State-specific nuances | Knowing your state’s rules and common damage types helps tailor your documentation for stronger claims. |

| Professional support helps | Working with expert public adjusters ensures your documentation and negotiations maximize your settlement. |

The core purpose of public adjuster documentation and what it includes

Understanding what documentation aims to accomplish is the foundation before diving deeper into its structure.

Public adjuster documentation is not about generating paperwork. It is about building an evidence chain that is clear, organized, and defensible. As one industry resource explains, a public adjuster’s documentation emphasis is less about “having paperwork” and more about creating an auditable, navigable evidence chain. Every item in the file needs to connect to the next so that anyone reviewing it, including your insurance carrier or an arbitrator, can follow the logic of your claim from start to finish.

When you look at a well-organized public adjuster file, you will typically find the following core document types:

- Photographs with timestamps and GPS-embedded metadata showing pre-loss condition and all areas of damage

- Incident reports documenting the date, time, nature, and initial scope of the loss event

- Weather data and meteorological reports confirming the storm event and its severity in your specific location

- Contractor and specialist estimates with itemized labor, materials, and scope explanations

- Policy review notes cross-referencing your coverage terms against the documented damage

- All correspondence between you, your carrier, and your public adjuster, logged chronologically

These elements work together. If your residential claims involve both interior and exterior storm damage, each affected area needs its own photo set, its own scope line in the estimate, and a clear connection back to the reported incident. That connection is what gives the file its credibility.

The goal of a structured claim file is not to impress the insurance company with volume. It is to give them no room to question the facts.

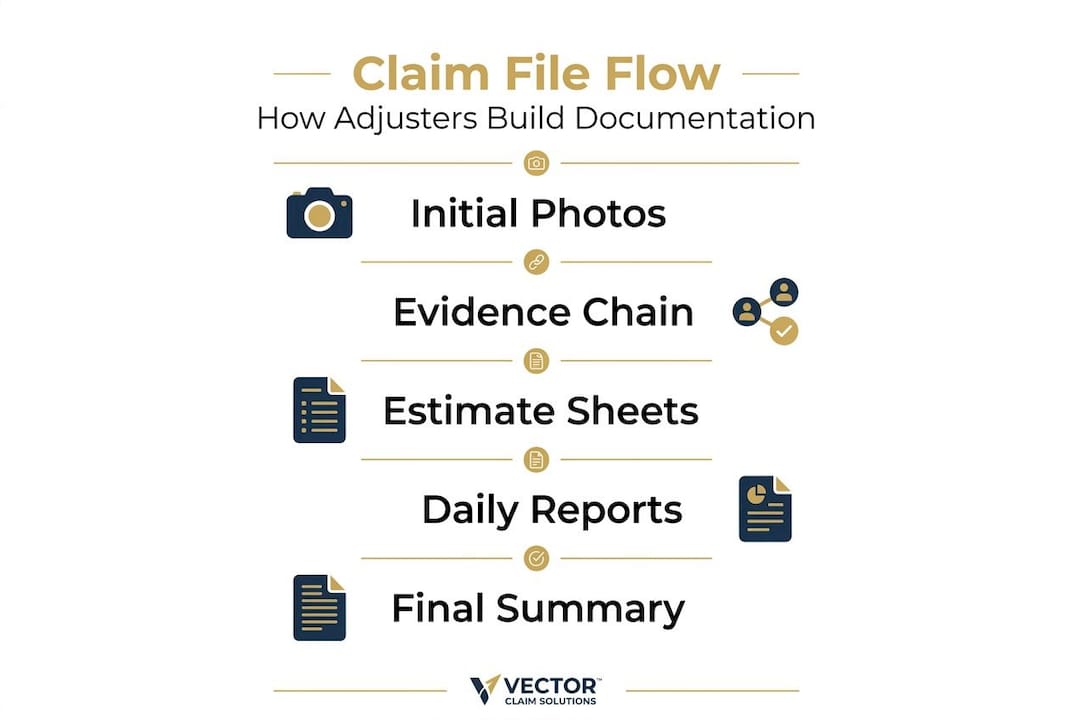

How a typical public adjuster file is organized: chronology, evidence, and estimate details

Having defined what the files contain, let’s explore how the documentation is precisely arranged to maximize claim credibility.

Chronological order is not optional in public adjuster documentation. It is the backbone of the entire file. The claim’s chronology shapes how the evaluation unfolds, and a well-managed chronology supports consistency and smoother resolution. Here is the sequence a properly structured file follows:

- Date of loss record with incident report and initial photos taken on the day of the event

- Immediate mitigation documentation showing emergency repairs taken to prevent further damage

- Weather corroboration tied specifically to the date and location of your property

- Inspection records from both your public adjuster and any specialist brought in for structural or roofing review

- Detailed damage estimate with itemized scope, unit costs, and material specifications

- Carrier correspondence log tracking all communications, responses, and deadlines

- Supplemental documentation added as additional damage is uncovered during repairs

Photos deserve special attention within that structure. They need embedded EXIF metadata, which is the technical term for the digital information stored in an image file that records the date, time, and GPS coordinates of when and where it was taken. Without that data, a photo is much harder to verify. This is not a minor detail. Documentation quality directly affects dispute risk and settlement speed, and carriers are increasingly scrutinizing files where documentation cannot stand up under examination.

Your storm damage checklist should account for every component below when building out the estimate section of your file:

| Estimate Component | What It Must Include |

|---|---|

| Scope of work | Every damaged area, system, or material listed separately |

| Labor costs | Trade-specific rates with hours justified by scope |

| Material costs | Current pricing with named product specifications |

| Scope rationale | Explanation of why each repair is necessary |

| Exclusions noted | Items reviewed but not claimed, with reasoning |

Pro Tip: Before your public adjuster submits the estimate, ask them to walk you through how each line item ties back to a specific photo or inspection note. If there is no direct link, that gap can be used against your claim.

Common documentation pitfalls and how to avoid them

Now that we know how documentation should be structured, it is important to also highlight common mistakes and how to avoid them to protect your claim.

The most damaging errors in public adjuster documentation are often the simplest ones. Claims are most commonly denied for lack of contemporaneous documentation, conflicting records, and late reporting. “Contemporaneous” means created at the time of the event, not reconstructed afterward. If you write up an incident summary three weeks after the storm, it carries far less weight than a report filed the same day.

Here are the most frequent mistakes property owners and their adjusters make, and what to do instead:

- Reconstructing records after the fact. Document on the day of loss. Date and timestamp everything in real time.

- Leaving gaps in the daily log. If your adjuster is on-site, there should be a note for every active work day. A gap of even two or three days raises questions about what happened during that period.

- Photos without metadata. Use a phone or camera that embeds GPS and timestamp data. Turn off any settings that strip this information.

- Inconsistent damage descriptions. If your incident report says the roof was damaged on the south slope but your estimate covers the north slope too, you need a supplemental report explaining why. Unexplained inconsistencies are red flags for carriers.

- Missing third-party corroboration. Weather reports, municipal damage records, and neighbor affidavits all strengthen your file. Do not skip them.

A claim file is only as strong as its weakest document. One inconsistent report can cast doubt on an otherwise solid file.

When you need guidance on how to navigate a property insurance claim correctly from the start, getting the documentation structure right from day one is non-negotiable. Reviewing your file against your policy’s covered claim types early in the process also prevents scope mismatches that slow settlements down.

Pro Tip: Use a free app that logs GPS-tagged photos directly into a cloud folder. This creates a tamper-evident record that is far more persuasive than photos uploaded from a personal camera roll later.

Practical steps for property owners: assembling and managing your documentation effectively

With common pitfalls addressed, let’s focus on concrete steps you can take right now to build effective documentation supporting your claim.

The window immediately after a storm is your most important documentation period. Most property owners underestimate how quickly conditions change, repairs begin, and memories fade. Here is a clear process to follow:

- Start photographing immediately. Cover every area of visible damage, the surrounding property, and even items that appear undamaged but may show wear later. More angles, not fewer.

- File your incident report the same day. Note the time, nature of the storm or event, and the specific damage you observed. Be factual, not speculative.

- Gather witness information. If neighbors or contractors observed the storm or the damage, collect their names and contact details.

- Pull weather data for your zip code. Services that provide historical storm records tied to your address and date are valuable corroboration tools.

- Create a dedicated folder structure. Organize files by date and category from day one. Do not let photos pile up in a generic camera roll.

- Log every conversation with your carrier. Write down who you spoke to, when, and what was said. Follow up phone calls with a brief email summary so there is a written record.

Every report has a verified creation timestamp that cannot be backdated, and digital reports create an audit trail showing when entries were created, modified, and submitted. This is exactly why digital tools matter so much. A handwritten note has no timestamp. A cloud-based report does.

Here is a quick reference for the documentation categories you need organized in your file:

| Documentation Type | Purpose in Claim File |

|---|---|

| Date-of-loss photos | Establishes extent and immediacy of damage |

| Incident report | Creates the official starting point of the claim |

| Weather records | Corroborates storm event and severity |

| Daily logs | Shows continuous, real-time tracking |

| Adjuster correspondence | Documents all carrier interactions |

| Contractor estimates | Quantifies repair scope and costs |

If you are dealing with storm damage claims, your public adjuster should be guiding you through each of these steps. When contractors are involved in repairs, make sure they understand their documentation responsibilities as well, as their records become part of your claim file. Learn more about working with contractors during the claims process.

Pro Tip: Ask your public adjuster for a weekly documentation summary during active claims. It keeps you informed and creates a record showing the claim was managed actively throughout.

How different states’ conditions affect public adjuster documentation needs

Now that you have practical steps, it is crucial to know how your state’s specific conditions influence how documentation should be handled.

Public adjuster documentation follows core principles everywhere, but state-specific rules and common damage types genuinely change how your file should be built. A qualified public adjuster has specialized expertise that can simplify and speed up the complicated process for settling claims from events like windstorm, hail, floods, and hurricanes, and that expertise must reflect regional knowledge.

Here is how documentation needs differ across the states we serve:

| State | Common Claim Types | Key Documentation Considerations |

|---|---|---|

| Texas | Hurricane, hail, wind | PA fees capped at 10% of settlement; strict timelines for filing |

| Florida | Hurricane, flood, water intrusion | Detailed flood zone documentation; strict post-hurricane deadlines |

| Nebraska | Hail, tornado, agricultural impact | Crop and structure overlap; tornado path documentation often needed |

| Iowa | Hail, flood, straight-line wind | FEMA flood map corroboration; neighbor impact records valuable |

| Colorado | Hail, snow load, wind | Hail size documentation critical; snow load structural reports common |

Beyond the table, there are a few state-specific points worth knowing:

- Texas requires public adjusters to be licensed under the Texas Department of Insurance and operates under specific fee cap rules. Your documentation file needs to reflect settlement figures accurately since fees are calculated against them.

- Florida has seen increasing post-hurricane claim disputes, which means your documentation must be airtight before submission. Supplemental claims face extra scrutiny.

- Colorado hail claims, especially from the Front Range corridor, frequently require hail size verification from weather data sources, as carrier inspectors sometimes contest storm severity.

- Nebraska and Iowa storm claims often involve large commercial or agricultural properties where damage scope is substantial. Commercial claims in these states benefit from documentation that addresses both structural and operational impact.

Always review your state’s filing deadlines early. Missing a statutory deadline can limit your claim options regardless of how strong your documentation is. Use a detailed storm damage claim checklist tailored to your region as your starting point.

Why the conventional paperwork mindset misses the real power of public adjuster documentation

Here is something worth sitting with: most property owners approach documentation by asking “how much do I need?” That is the wrong question entirely.

Volume does not win claims. Continuity does. Structure does. Verifiability does. We have seen files with hundreds of photos that were nearly useless because nothing was labeled, timestamped, or connected to the estimate. And we have seen lean, well-organized files that settled quickly and at full value because every single item supported the next.

Documentation is the lifeblood of the claims process, and the integrity of the documentation matters as much as the documents themselves. The sequence in which information is added contributes to a credible and persuasive claim file. That is not bureaucratic language. It means that a photo taken on the day of loss is worth exponentially more than the same photo taken two weeks later, even if the damage is identical.

The adjuster who builds a file that reads like a clear timeline, supported by real-time records and consistent damage descriptions across every document, gives the carrier nothing to argue with. That is the real goal. Not more paper. A better-constructed case.

Understanding how insurance calculates claim payments also reframes how you think about documentation. Every line item in your estimate needs a documented reason to exist. If the documentation does not support a repair, the carrier will not pay for it. Approaching your file with that logic, rather than hoping volume creates credibility, changes your outcomes significantly.

How Vector Claim Solutions supports your claim through expert documentation and negotiation

Understanding how public adjuster documents are structured is one thing. Executing it under the stress of a storm loss is another.

At Vector Claim Solutions, we build claim files that insurers take seriously. Our team manages every layer of the adjuster claims documentation process, from same-day loss reporting through final settlement negotiation, so nothing falls through the cracks. We understand the regional nuances that affect claims in Nebraska, Iowa, Colorado, Texas, and Florida, and we apply that knowledge to every file we manage. If you are unsure whether your current documentation is strong enough, or you suspect your claim was undervalued, we can review your estimate with no pressure. Learning more about why a public adjuster for storm claims makes sense is a good place to start. We are here to make sure your insurance claim payment reflects the full, actual cost of restoring your property.

Frequently asked questions

Why is structured documentation so important in insurance claims?

Structured documentation ensures your claim is clear, evidence-based, and credible, which speeds resolution and reduces dispute risk. Documentation quality directly affects dispute risk and settlement speed, and files that cannot withstand scrutiny are far more likely to be contested.

What kinds of photos are needed for a public adjuster’s file?

Photos with embedded metadata showing date, time, and GPS location from multiple angles before and after damage are essential. Photos with embedded EXIF metadata showing date, time, and GPS coordinates are far more credible than images without that data.

Can missing daily reports hurt my claim?

Yes, gaps in daily reports can raise doubts about your documentation’s credibility and may delay or reduce your settlement. Claims supported by a continuous chain of daily reports are dramatically more credible than one-off reports created specifically for the claim.

Are public adjusters’ fees capped in all states?

Fee caps vary by state. In Texas, for example, a public adjuster’s fee is capped at 10% of the claim settlement, which is a specific regulatory rule that affects how claims are valued and negotiated.

How do state differences affect public adjuster documentation?

Each state has unique rules and common damage types, so documentation must match regional claim protocols and timelines for the best results. A qualified public adjuster’s specialized expertise in regional claim types such as hail, floods, and hurricanes can significantly simplify and speed up your settlement.