When your insurance company denies your claim or offers a settlement that barely covers your repair costs, it can feel like the decision is final. It is not. Many homeowners and commercial property owners walk away from money they are rightfully owed simply because they do not know that a structured appeal process exists. In reality, insurers are required to review written appeals, and there are clear steps you can follow to challenge a denial or underpayment. This guide walks you through each stage of the property claim appeal process, explains what evidence matters most, and shows you how to escalate when the first appeal is not enough.

Table of Contents

- Understanding claim denials and why appeals happen

- Step-by-step: The property claim appeal process

- Key components: Documentation, deadlines, and policy language

- Appraisal, state complaints, and next-level dispute options

- A seasoned perspective: What most policyholders miss about appeals

- Need expert help with your insurance claim appeal?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Appeals are not final denials | Insurance claim denials or underpayments can be challenged through a structured appeal process. |

| Document everything | Clear, comprehensive evidence and careful review of your policy increase your chance of a successful appeal. |

| Multiple resolution pathways | Options like appraisal, state complaints, and legal remedies exist if your initial appeal is unsuccessful. |

| Deadlines are critical | Missing documentation or submitting late can undermine even a strong appeal. |

Understanding claim denials and why appeals happen

Now that you know a denied or underpaid claim is not the final answer, let’s clarify what triggers the need for an appeal and why insurance companies allow this process.

A claim denial means your insurer has decided your loss is not covered under your policy. An underpayment means the insurer acknowledges the loss but offers a settlement amount that does not reflect the actual cost to repair or replace the damaged property. Both outcomes can be disputed, and both are more common than most policyholders realize.

Here are the most frequent reasons insurers deny or underpay property claims:

- Coverage exclusions: The insurer argues the cause of damage is excluded from your policy. Flooding, for example, is commonly excluded from standard homeowners policies.

- Insufficient documentation: The claim file lacks the photos, estimates, or reports needed to support the loss.

- Missed deadlines: Policyholders sometimes wait too long to report damage or submit required paperwork.

- Policy lapses or non-payment: If your premium was not current at the time of the loss, the insurer may deny the claim outright.

- Disputed cause of loss: The insurer’s adjuster attributes damage to wear and tear or pre-existing conditions rather than a covered event like hail or wind.

- Scope disagreements: The insurer’s estimate covers only part of the damage, leaving out items that a thorough inspection would have caught.

Understanding common denial reasons is the first step toward building a strong appeal. If you know exactly why the claim was denied, you can address each reason directly.

For U.S. homeowners and commercial property policies, an appeal of a denied or underpaid property claim usually starts with an internal, written reconsideration to the insurer, using the denial letter and policy language as the roadmap.

The denial letter is your most important starting document. It tells you exactly what the insurer objected to, which policy language they relied on, and what evidence they say was missing. Reading it carefully, alongside your actual policy, is essential before you write a single word of your appeal. If you need a broader foundation for this process, reviewing navigating a property claim from the beginning can give you important context.

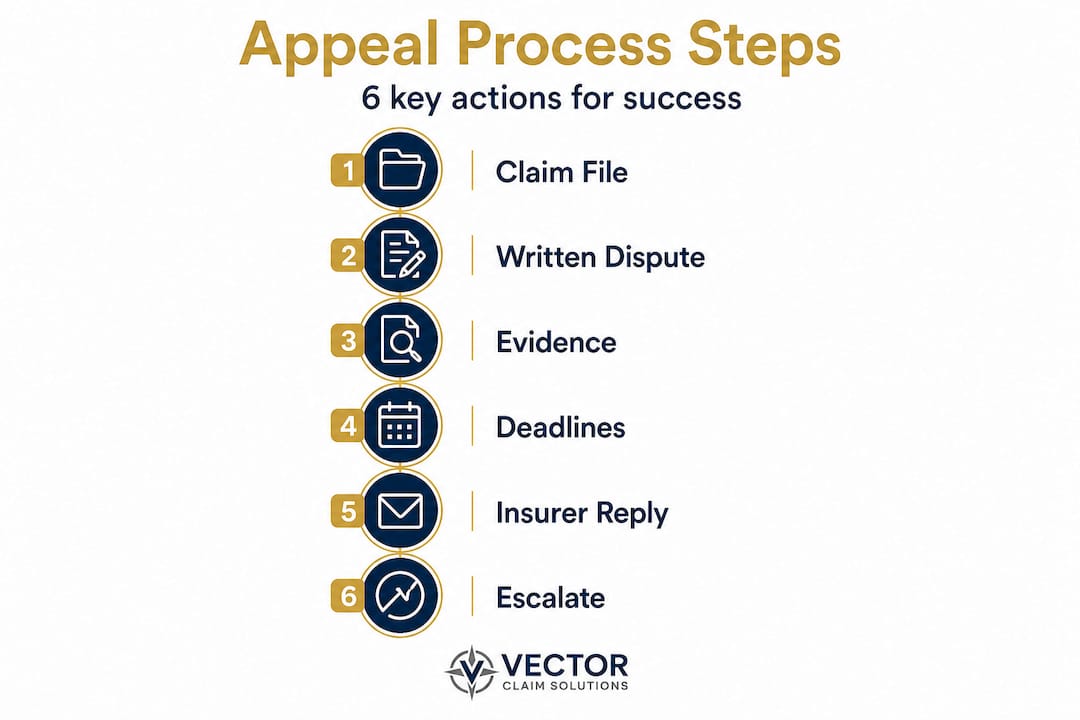

Step-by-step: The property claim appeal process

With the reasons for denials in mind, let’s break down exactly how the appeal process unfolds and what you need at every stage.

Step 1: Request your complete claim file

Before you write your appeal, request a full copy of your claim file from the insurer. This includes the adjuster’s notes, photos taken during the inspection, and any internal communications. You are entitled to this information, and it often reveals gaps or errors in how the claim was evaluated.

Step 2: Write a formal, written dispute

Your appeal must be in writing. Address each denial reason individually, referencing specific policy language and the evidence that counters the insurer’s position. Vague objections do not work. Be specific, factual, and organized.

Step 3: Assemble your evidence package

Appeal documentation typically includes a clearly written dispute of each denial reason and an evidence package with photos, repair estimates, and relevant policy excerpts. Your evidence package should include:

- Dated photographs of all damage

- A repair or replacement estimate from a licensed contractor

- Excerpts from your policy that support coverage

- Any expert reports, such as a structural engineer’s assessment or a public adjuster’s scope of loss

- A timeline of events showing when the damage occurred and when it was reported

Step 4: Submit within the required timeframe

Most policies include deadlines for filing appeals. Missing these deadlines can forfeit your right to dispute the decision. Check your policy and the denial letter carefully for any stated timeframes.

Step 5: Wait for the insurer’s response

After submitting your appeal, the insurer is required to respond within a timeframe set by state law. This varies by state but is commonly 30 to 45 days. Keep copies of everything you submit and note the date you sent it.

Step 6: Escalate if the appeal is denied

If the internal appeal does not succeed, you have additional options. Filing a complaint with your state insurance department triggers a formal investigation and requires the insurer to respond to a regulator. This step alone often motivates insurers to reconsider their position.

Pro Tip: Send your appeal via certified mail with return receipt requested. This creates a paper trail that proves the insurer received your dispute, which matters if you need to escalate later.

The table below summarizes each stage and what to expect:

| Stage | Action required | Expected timeline |

|---|---|---|

| Internal appeal | Written dispute with evidence package | 30 to 60 days for insurer response |

| State department complaint | Formal complaint filed with regulator | 30 to 90 days depending on state |

| Appraisal | Independent appraisers assess value | 30 to 90 days |

| Mediation | Neutral third party facilitates negotiation | Varies |

| Arbitration or litigation | Formal legal process | Months to years |

If you are concerned that your settlement offer is too low, reviewing undervalued claim estimates can help you identify specific shortfalls before you write your appeal.

Key components: Documentation, deadlines, and policy language

Understanding the official steps is only part of the puzzle. Effective appeals depend on strong documentation and meeting all deadlines.

Reading your denial letter correctly

The denial letter is a legal document. Every sentence matters. Look for the specific policy exclusion or condition the insurer cited, the exact language used to justify their decision, and any reference to missing documentation. If the letter is vague, write back and ask for clarification in writing. Insurers are required to explain their decisions clearly.

Locating and using your policy language

Your policy is a contract. If the insurer says a loss is excluded, find the exclusion yourself and read the full context. Many exclusions have exceptions, and many policyholders miss coverage they actually have. Pay attention to definitions within the policy, because words like “occurrence,” “sudden,” and “direct physical loss” have specific legal meanings that can affect whether your claim is covered.

Additional evidence that strengthens appeals

Beyond photos and estimates, the following types of evidence can significantly improve your appeal:

- Independent contractor estimates: An estimate from a contractor you hire yourself often reflects true repair costs more accurately than the insurer’s preferred vendor.

- Public adjuster scope of loss: A licensed public adjuster can produce a detailed, line-by-line scope of damage that counters the insurer’s assessment.

- Meteorological reports: For storm damage claims, weather data confirming hail size, wind speed, or storm timing on the date of loss is powerful supporting evidence.

- Building code documentation: Local building codes may require upgrades during repairs that the insurer’s estimate does not account for.

- Expert reports: Engineers, roofing specialists, or other licensed professionals can provide written opinions that directly challenge the insurer’s findings.

What to collect for an appeal is a process that takes time, but the quality of your documentation is often the deciding factor in whether your appeal succeeds.

Deadlines you cannot afford to miss

Most policies include a “suit limitation” clause, which sets a deadline for filing a lawsuit if all else fails. This is typically one to two years from the date of loss, though it varies by state and policy. Internal appeal deadlines are usually shorter. Missing any of these deadlines can permanently eliminate your right to recover additional funds.

Pro Tip: Create a simple spreadsheet tracking every deadline, submission date, and insurer response. This keeps you organized and gives you a clear record if the dispute escalates to a regulator or court.

Appraisal, state complaints, and next-level dispute options

If your initial appeal does not succeed or if your dispute is about the claim’s value or coverage terms, several alternative pathways exist to continue your fight.

Understanding appraisal vs. coverage disputes

This distinction is critical and often misunderstood. Many property policies include an appraisal clause that applies to disputes over the amount of loss, not necessarily whether the loss is covered. In other words, if you and the insurer agree the damage is covered but disagree on the dollar value, appraisal may be your fastest path to resolution.

However, appraisal is commonly aimed at disagreements about the dollar value of a covered claim, while coverage disagreements require internal appeal, a state department complaint, and sometimes legal remedies rather than appraisal alone. Knowing which type of dispute you have determines which path to take.

How the appraisal process works

In a formal appraisal:

- You hire a licensed appraiser to represent your interests

- The insurer hires their own appraiser

- Both appraisers agree on a neutral umpire

- The umpire resolves any differences between the two appraisers’ findings

- The resulting award is typically binding on both parties

Appraisal is faster and less expensive than litigation, but it works only for valuation disputes. It will not resolve a dispute about whether a peril is covered.

Filing a state insurance department complaint

Every state has a Department of Insurance (DOI) that regulates how insurers handle claims. Filing a complaint is free and relatively straightforward. You submit your complaint online or by mail, include copies of your denial letter and appeal correspondence, and describe the specific issue. The DOI then contacts the insurer and requires a formal response. This process often prompts insurers to take a second, more careful look at disputed claims.

Mediation, arbitration, and litigation

- Mediation: A neutral mediator helps both sides negotiate a settlement. It is non-binding, meaning either party can walk away.

- Arbitration: A neutral arbitrator hears both sides and issues a decision. Depending on your policy, this may be binding.

- Litigation: Filing a lawsuit is the most time-consuming and expensive option, but it may be necessary for large losses or bad faith conduct by the insurer.

If you are unsure which path fits your situation, when to seek help with disputes is a useful resource. For business owners, understanding the commercial claims process adds important context for larger or more complex disputes.

A seasoned perspective: What most policyholders miss about appeals

After working through hundreds of disputed claims, a pattern becomes clear. Most policyholders do not lose their appeals because the insurer is right. They lose because they made avoidable mistakes in how they prepared and presented their case.

The most common mistake is submitting an appeal that is too general. Writing “I disagree with your decision” and attaching a few photos is not an appeal. It is a complaint. A real appeal addresses each denial reason with specific policy language, specific evidence, and a clear explanation of why the insurer’s position is incorrect. Specificity wins disputes.

The second mistake is choosing the wrong dispute path. If your issue is about the dollar value of a covered loss, appraisal is often faster and more effective than a state complaint. If your issue is about whether the loss is covered at all, appraisal will not help you. Matching your strategy to the actual dispute type is something many policyholders overlook, and it costs them time and money.

The third mistake is waiting too long. Deadlines in insurance policies are real and enforceable. We have seen policyholders with strong cases lose their right to recover simply because they missed a filing deadline by a few weeks. Start the process as soon as you receive a denial or a settlement offer that does not cover your actual costs.

Finally, many policyholders underestimate what a licensed public adjuster brings to an appeal. A public adjuster works exclusively for you, not the insurer. They know how to document damage at a construction level, how to read policy language, and how to negotiate with carriers. On complex claims involving different claim types like storm, water, or large commercial losses, professional representation often results in significantly higher settlements than policyholders achieve on their own.

The uncomfortable truth is that insurance companies have experienced adjusters, attorneys, and claims teams working on their side. You deserve equally experienced representation on yours.

Need expert help with your insurance claim appeal?

If the appeals process seems daunting or you want the best chance at a fair outcome, professional support can make all the difference.

At Vector Claim Solutions, we work exclusively for policyholders. Whether you are dealing with a denied homeowners claim or a complex commercial loss, we know how to build the documentation, analysis, and negotiation strategy that gets results.

Our residential claim experts and commercial claim adjusters have guided property owners through every stage of the appeal process, from internal reconsiderations to state complaints and appraisal. We help you understand what your policy actually covers, what your damage actually costs, and how to maximize your settlement with precision and persistence. Reach out today for a claim review and take the first step toward a fair resolution.

Frequently asked questions

How long does the property claim appeal process typically take?

Most internal insurance claim appeals are resolved in 30 to 60 days, but timelines vary by insurer and state rules. Escalation to a state department complaint or appraisal can add several additional months.

What documents are most important to include with my appeal?

Always include your denial letter, relevant policy pages, evidence of damage such as photos, and repair estimates. Appeal documentation should also include a clearly written dispute of each denial reason for the strongest possible case.

When should I file a complaint with my state insurance department?

File a complaint after you have completed your insurer’s internal appeal and still disagree with their decision. State department complaints trigger a formal investigation and require the insurer to respond to a regulator.

Does the appraisal process cost extra and do I need a lawyer?

Appraisal costs usually involve fees for appraisers and the umpire, but you do not always need a lawyer. Appraisal clauses apply specifically to disputes over the amount of loss, not coverage questions, so complex coverage disputes may benefit from legal advice.

Can public adjusters help with the appeal process?

Yes, public adjusters can prepare and present your appeal, assist with evidence gathering, and negotiate directly with the insurer on your behalf. They are especially valuable on large or complex claims where the documentation and negotiation demands go beyond what most policyholders can manage alone.