One of the most common reasons hail damage claims stall or get denied has nothing to do with the severity of the damage. It comes down to a single detail: the confirmed storm date. Understanding how hail storm date confirmed for claims purposes is established separates policyholders who receive full settlements from those who end up in protracted disputes with their insurer. Whether you own a single-family home in Nebraska or manage a commercial property in Texas, knowing how to pin down the right storm date, and document it credibly, is the foundation of every successful hail claim.

Table of Contents

- Key takeaways

- Why the storm date matters for your claim

- Tools and methods for confirming hail storm dates

- Storm date disputes and how they complicate claims

- Step-by-step guidance for documenting and confirming your storm date

- My take on why early confirmation changes everything

- How Vectorclaimsolutions can help you confirm dates and file correctly

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Storm date anchors your claim | The confirmed hail date sets deadlines, establishes coverage eligibility, and drives the entire hail storm claim process. |

| Use property-specific data | Regional weather reports alone are not enough. Address-specific radar data is required to confirm storm date accurately. |

| File promptly | Most policies require filing within 1 year of the storm. Delays increase the risk of denial and reduced payouts. |

| Align all experts early | Your adjuster, roofer, and meteorologist must agree on the storm date before you file to avoid theory-of-loss disputes. |

| Documentation is your defense | Photos, inspection reports, and weather records collected quickly give your claim the best chance of a full settlement. |

Why the storm date matters for your claim

When you file a hail damage insurance claim, the date of loss is not just a formality. It is the legal anchor for your entire claim. Your insurer uses the storm date to verify that the damage occurred during an active policy period, calculate any depreciation, and determine whether you filed within the required timeframe.

Most homeowners must file within one year of the storm event, though some state laws extend that window to two years. If you miss that deadline, your claim can be denied regardless of how legitimate the damage is. That is a serious risk, especially in regions like Colorado and Iowa where multiple storms can hit within the same season and homeowners sometimes realize the damage months later.

The storm date also matters because it triggers depreciation calculations. The longer you wait after the storm, the more your insurer may apply depreciation to materials and labor. And if secondary damage develops, such as a roof leak causing interior water damage, the insurer may dispute whether that secondary damage stems from the original hail event or from neglect.

Here is why the date is so high stakes for policyholders:

- Coverage eligibility: Your policy must have been active on the storm date, or the claim has no basis.

- Filing deadlines: Missing the deadline, even by days, gives the insurer grounds for denial.

- Depreciation exposure: Earlier filing typically results in less depreciation applied to your settlement.

- Secondary damage attribution: A confirmed storm date helps connect follow-on damage to the original event.

Hail-related claims represent about 31% of claim volume across the country, making this one of the most frequently disputed claim types in the industry. Knowing what date to use is not a detail you can afford to get wrong.

Tools and methods for confirming hail storm dates

The good news is that confirming the correct storm date is more reliable than most homeowners realize. There are multiple professional-grade resources available, and combining them is the key to a defensible answer.

NOAA and the National Weather Service maintain public archives of severe weather events, including storm paths, hail reports, and event timing. The NOAA Storm Events Database is a starting point, but it records storm reports at a regional or county level, not at the address level. That distinction matters more than most people expect.

Radar-based hail verification tools fill that gap. Services like HailScore and similar platforms use NOAA-derived radar data to map confirmed hail events to specific street addresses. These reports typically include hail size, storm duration, and the exact path the storm traveled. This is the kind of address-specific evidence that carries real weight during the hail storm claim process.

Forensic meteorologists represent the gold standard for disputed claims. A forensic meteorologist analyzes radar signatures, storm reports, and surface observations to determine whether a hail-producing storm actually affected your property at a specific time. Their conclusions are framed in terms of probability and consistency with multiple data layers, which is exactly what insurers and courts need to see.

However, there is one critical caveat. Radar-derived hail size estimates indicate potential severity but do not directly measure what landed on your roof. A roof inspection is still required to correlate observed damage with the storm data, connecting the meteorological record to your specific property.

Common mistakes in date confirmation include:

- Relying on a neighbor’s recollection or a local news report as the only source

- Using a county-level storm report when address-specific radar data is available

- Assuming one storm report covers the entire neighborhood without checking property-specific records

- Waiting too long to pull records, since some data archives become harder to access over time

Pro Tip: Run an address-specific hail lookup immediately after a suspected storm event. Free tools exist, but paid reports from professional verification platforms provide the documentation detail that insurers take seriously.

Storm date disputes and how they complicate claims

Even with good data, storm date disputes happen. And when they do, the consequences for your claim can be significant.

The most common scenario involves multiple storms in a single season. If your area was hit by hail in April, June, and September, and you notice damage in October, both you and your insurer may disagree about which storm caused the damage. Legal conflicts increasingly involve technical assessments of roof damage and disputed storm dates, and insurers are more aggressive than ever about these disputes.

Here is how disputes typically develop and what you need to know about resolving them:

- The insurer questions the date of loss. They may argue the damage predates your current policy or stems from a storm that occurred before your coverage began.

- Damage pattern analysis becomes contested. A professional roof inspection can show whether damage characteristics match a specific hail size and storm event, but if the inspection happens months after multiple storms, the analysis gets complicated.

- Expert opinions diverge. If your adjuster points to one storm date and a roofing contractor points to another, you have a problem. Uncoordinated storm date opinions create what claims professionals call a “theory-of-loss” problem, and it can be nearly impossible to resolve once a claim is filed.

- The insurer uses the discrepancy to deny or reduce the claim. Even if your damage is real, conflicting dates give the insurer a technical basis to dispute coverage.

“Filing a claim without consensus on storm date between your experts can create irreparable theory-of-loss problems that become extremely difficult to resolve during litigation.” — Property Insurance Coverage Law Blog

The way to avoid this is to align your meteorologist, roofing inspector, and public adjuster on the storm date before you file. Early coordination is not optional. It is a prerequisite for a clean claim.

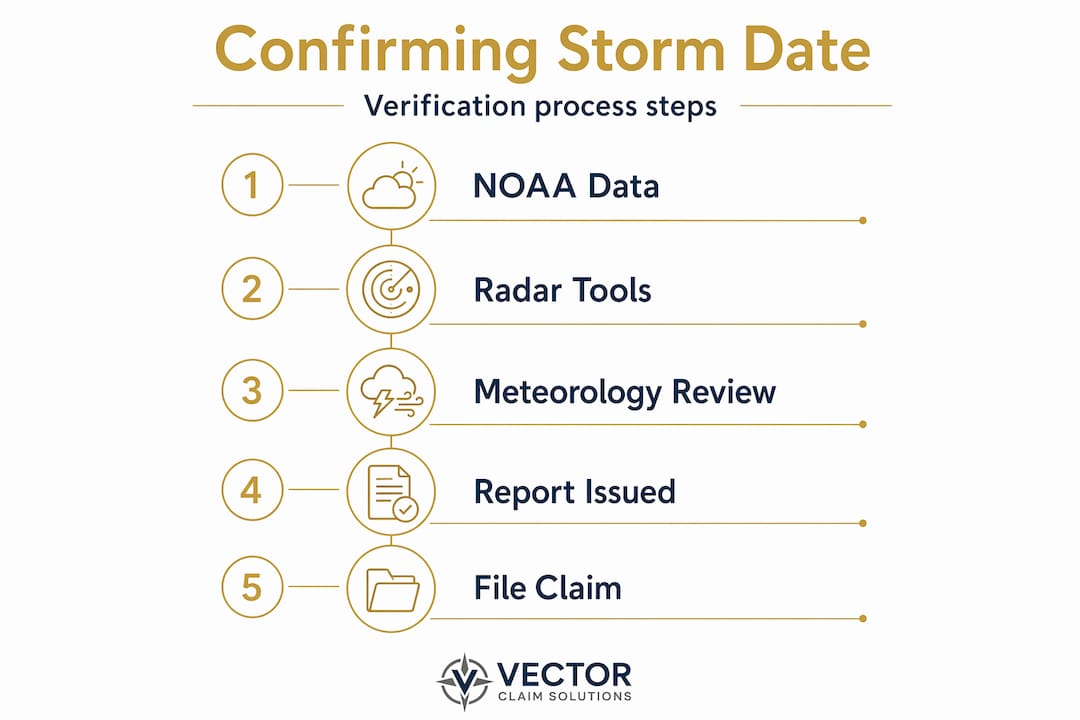

Step-by-step guidance for documenting and confirming your storm date

You do not need to be an insurance professional to take the right steps after a hailstorm. What you need is a clear process and the discipline to follow it quickly.

-

Conduct an immediate post-storm visual inspection. Walk your property within 24 to 48 hours of the storm. Look for dented gutters, bruised shingles, cracked skylights, and damage to AC units or exterior vents. Photograph everything with timestamps enabled on your device.

-

Run an address-specific hail lookup. Use a hail verification tool to pull radar-confirmed storm data for your exact address. Note the storm date, reported hail size, and storm path. Save this report.

-

Schedule a professional roofing inspection promptly. Inspections within 30 to 60 days post-storm receive more favorable responses from insurers. A qualified roofing inspector can document damage characteristics that correlate with the confirmed storm date. Use a hail damage inspection checklist to prepare for that inspection and make sure nothing is missed.

-

Coordinate weather data with your inspection report. Before contacting your insurer, compare the inspection findings with the radar data. The damage size, pattern, and location should be consistent with the storm’s confirmed hail size and path. If they are not, you need to understand why before filing.

-

Report the damage to your insurer with a confirmed date. When you contact your insurer to open a claim, use the date from your radar-verified storm report. Do not guess, and do not use a range of dates. A single, well-documented date of loss is far stronger than “sometime in June.”

-

Maintain a documentation file throughout the claim process. Keep all photos, storm reports, inspection results, insurer correspondence, and repair estimates in one organized place. Accurate storm event documentation is what separates settled claims from disputed ones.

Pro Tip: If you manage multiple properties, set up a standing protocol to pull hail reports for all addresses within 48 hours of any regional storm event. Waiting until you notice damage means waiting too long.

My take on why early confirmation changes everything

I’ve worked enough hail claims to tell you that delay is the single biggest threat to your settlement. Not the damage itself. Not the insurer. The delay.

I’ve seen cases where a homeowner waited eight months to file because they were unsure which storm caused the damage. By that point, we were dealing with degraded physical evidence, missing weather archive access, and an insurer who had every reason to question the date of loss. Situations like that can be salvaged, but they take far more work and produce worse outcomes than if the policyholder had acted in the first 60 days.

What I’ve learned from reviewing disputed hail claims across Nebraska, Iowa, Colorado, Texas, and Florida is that the policyholders who do well are the ones who treat the storm date like a legal document from day one. They pull radar data immediately. They get a roof inspection on the calendar before the week is out. They don’t file until their roofer and their weather data agree.

The NOAA Storm Events Database combined with radar and local reports gives you a solid foundation, but it still needs a trained eye to connect weather evidence to physical damage. That is where professional help pays for itself many times over. Policyholders who bring in a public adjuster early in the process almost always have cleaner documentation, fewer disputes, and faster resolution. That’s not a pitch. That’s just what the evidence shows.

— Vector

How Vectorclaimsolutions can help you confirm dates and file correctly

When a hailstorm hits your property, knowing where to start and who to trust makes a real difference. Vectorclaimsolutions works directly with homeowners and property managers to confirm storm dates, coordinate inspection reports, and document damage in a way that supports a full and fair settlement.

We specialize in hail, wind, water, and large-loss commercial claims across Nebraska, Iowa, Colorado, Texas, and Florida. If you have already filed and received a low estimate, or if you are trying to determine whether your damage qualifies for a claim, we can review your situation and tell you exactly where you stand. Understanding how insurance calculates claim payments is often the first step toward recovering what you are actually owed. You can also explore our hail damage claims services for a detailed look at what a professionally managed claim looks like. Reach out to Vectorclaimsolutions for a no-pressure review of your claim or estimate.

FAQ

How is hail storm date confirmed for an insurance claim?

Storm date confirmation uses radar-verified hail data from tools like NOAA databases and address-specific hail reports, combined with a professional roof inspection that correlates physical damage to the confirmed storm event. Forensic meteorologists can provide formal analysis for disputed dates.

What if I’m unsure which storm caused my roof damage?

Pull address-specific hail reports for all storm events in the past year and have a professional roofer inspect the damage to determine which storm’s hail size and pattern matches the observed damage characteristics. Aligning this evidence before filing prevents theory-of-loss disputes.

How long do I have to file a hail damage claim?

Most homeowners have one year from the storm date to file, though some states allow up to two years. Check your policy language carefully, since missing the deadline is grounds for denial even when damage is legitimate.

Can I use a regional storm report as my storm date proof?

Regional or county-level storm reports are a starting point, but weather data must be property-specific to hold up under insurer scrutiny. Address-level radar data provides far stronger documentation for the hail damage insurance date on your claim.

What happens if my adjuster and roofer disagree on the storm date?

Conflicting expert opinions on the date of loss create a serious problem once a claim is filed. Coordinate all parties before you file, since unresolved disagreements on the storm date can result in partial payment, denial, or extended disputes that become difficult to resolve later.