After a hailstorm passes, most homeowners do a quick visual check, see no obvious holes or caved-in sections, and assume their roof made it through just fine. That assumption is one of the most costly mistakes you can make. Understanding why hail damage worsens over time is the difference between a repair that costs a few hundred dollars and a full roof replacement that your insurer may no longer feel obligated to cover. Damage that starts as invisible bruising and minor granule loss can quietly evolve into leaks, rot, and structural failure over months without a single visible warning sign.

Table of Contents

- Key takeaways

- Why hail damage worsens over time

- Factors that speed up the damage

- What happens when repairs are delayed

- How to detect, document, and respond quickly

- Hail damage vs. normal roof aging

- My take on early detection after years in the field

- Get help protecting your hail damage claim

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Damage is often invisible at first | Hail can bruise shingles and displace granules without leaving obvious punctures or holes. |

| Environmental stress accelerates failure | Freeze-thaw cycles, UV exposure, and rain seepage turn minor impacts into major structural problems. |

| Delays hurt your insurance claim | Evidence of hail damage fades within months, making it harder to prove a storm caused the damage. |

| Documentation timing is everything | Photographing damage within days of a storm protects both your property and your claim rights. |

| Early inspection prevents larger costs | Catching hail damage quickly limits repair scope and reduces the risk of a full replacement. |

Why hail damage worsens over time

Most people picture hail damage as visible dents, cracked shingles, or missing sections. The reality is far more subtle. Hail damage to asphalt shingles commonly appears minor at first, presenting as granule loss or bruising that accelerates shingle aging due to UV exposure and temperature cycling.

Here is what is actually happening beneath the surface when hail strikes your roof:

- Granule displacement: Each shingle is coated with protective granules that act as a barrier against the sun. When hail knocks them loose, the raw asphalt underneath is exposed directly to UV rays. That exposure starts a clock on premature deterioration.

- Fiberglass mat bruising: Beneath the granules and asphalt coating sits a fiberglass reinforcement mat. Hard hail impacts compress and crack this mat, even when the outer surface looks intact. The shingle may look fine from the ground but has lost meaningful structural strength.

- Soft metal impacts: Check your gutters, downspouts, and AC unit housing after any storm. Dings and dents on these softer surfaces are reliable indicators that hail was large enough to damage your roofing as well.

- Underlying deck vulnerability: Once the shingle layer is compromised, the wood decking beneath becomes susceptible to moisture even before a visible leak forms.

The deceptive part is that hidden material weaknesses caused by hail can lead to structural failures despite no obvious punctures. A roof that passes a casual visual inspection may already be on a path toward failure that will reveal itself in the next rain season or winter freeze.

Pro Tip: Run your hand along a suspect shingle after a storm. A healthy shingle feels firm and consistent. A bruised shingle may have a soft, spongy spot beneath an otherwise normal-looking surface.

Factors that speed up the damage

Once hail has compromised your roof’s protective layers, the environment takes over. The causes of worsening hail damage are almost entirely driven by the conditions your roof faces every single day after the storm.

Here is the sequence that plays out on most damaged roofs:

- UV degradation: Exposed asphalt dries out faster than protected shingles. Granule loss reduces shingle protection from sun and weather, causing exposed shingles to dry out, become brittle, and crack, eventually letting water seep into decking and causing rot and mold growth.

- Freeze-thaw cycles: Any crack or micro-fracture in a shingle absorbs water. When temperatures drop, that water freezes and expands, widening the crack. This cycle repeats throughout winter and early spring, progressively enlarging the damage with every freeze.

- Rain seepage: Water is patient. Once a crack or gap exists in your shingle layer, rain will find it. Interior leaks from hail damage often appear months after a storm because weakened roofing materials deteriorate slowly before allowing water penetration.

- Wind uplift: A shingle that was weakened at its bond point by a hail strike is far more susceptible to lifting in the next windstorm. Partial lifts allow more water intrusion and make further damage far more likely.

- Biological growth: Moisture trapped beneath compromised shingles creates an ideal environment for moss, algae, and mold. These organisms break down roofing materials further and can extend damage into the attic insulation and structural framing.

The long-term effects of hail damage are not theoretical. They follow a predictable path, and the further you get from the original storm without repairs, the more severe and expensive each stage becomes. Homeowners in states like Nebraska, Colorado, and Iowa face particularly aggressive freeze-thaw cycles that compress this timeline significantly.

What happens when repairs are delayed

Delaying repairs does not just affect your roof. It affects your insurance claim, your home’s value, and your out-of-pocket costs. The consequences compound quickly.

- Leaks appear months later: The delayed nature of hail-related leaks creates a genuine problem for homeowners. By the time water appears on your ceiling, the storm that caused it may have happened six months ago. Linking that water damage back to a specific hail event becomes much harder without early documentation.

- Claims face heightened scrutiny: Evidence like exposed asphalt mat loses its visual contrast due to oxidation after about six months, making older damage significantly harder to prove. Adjusters are trained to look for this, and aged damage frequently gets classified as pre-existing wear.

- Denial risk increases: Delayed hail damage claims run a higher risk of denial because documentation may not clearly link the damage timing and cause to a covered storm event.

- Repair costs escalate: Minor impact damage overlooked initially often turns into expensive repairs as leaks and rot develop. A targeted shingle repair that might have cost $800 becomes a full deck replacement once moisture penetrates the wood.

- Secondary damage claims get complicated: Water damage to your attic insulation, ceiling drywall, or interior finishes may be covered under your policy, but only if you can connect it to the original hail event. Without that documented chain of causation, your insurer may treat it as a separate, unrelated claim.

Pro Tip: Even if you choose not to file a claim immediately, have a professional inspection done within two weeks of any significant storm. A written inspection report creates a timestamped record that protects your ability to file later.

How to detect, document, and respond quickly

Acting within days of a hailstorm puts you in the strongest possible position, both for repairs and for your insurance claim. Here is a practical approach that Vectorclaimsolutions recommends to homeowners after any significant storm:

- Schedule a professional inspection promptly. Do not rely solely on your own visual assessment. A qualified roofing professional or public adjuster can identify bruising, granule displacement, and mat damage that is invisible from ground level. Use a hail damage inspection checklist to make sure nothing gets missed.

- Photograph everything systematically. Capture wide shots showing the full roof slope, then close-ups of individual impact points. Documenting varied hail hits and early granule loss signs helps prove damage recency and storm cause to insurers.

- Photograph soft metal surfaces. Dented gutters, downspouts, and metal vents provide compelling supporting evidence of hail size and intensity.

- Record the storm date and details. Note the date, time, and any weather service reports for your area. Your insurer will cross-reference your claim with meteorological data.

- Keep a damage journal. Write down when you first noticed each symptom, when you called for an inspection, and what the inspector found. This timeline becomes critical if your claim is disputed.

- Get a second opinion on your estimate. Insurance adjusters work for the carrier. A public adjuster works for you and may identify roof damage documentation opportunities that a carrier-appointed adjuster overlooks.

| Action | Ideal timing | Why it matters |

|---|---|---|

| Professional inspection | Within 14 days of storm | Captures fresh damage before oxidation begins |

| Photographic documentation | Within 48 hours | Preserves clear visual evidence of impact patterns |

| Filing notice of claim | Within 30 days | Meets most policy requirements for timely notification |

| Independent estimate review | Before accepting settlement | Confirms repair scope matches actual damage |

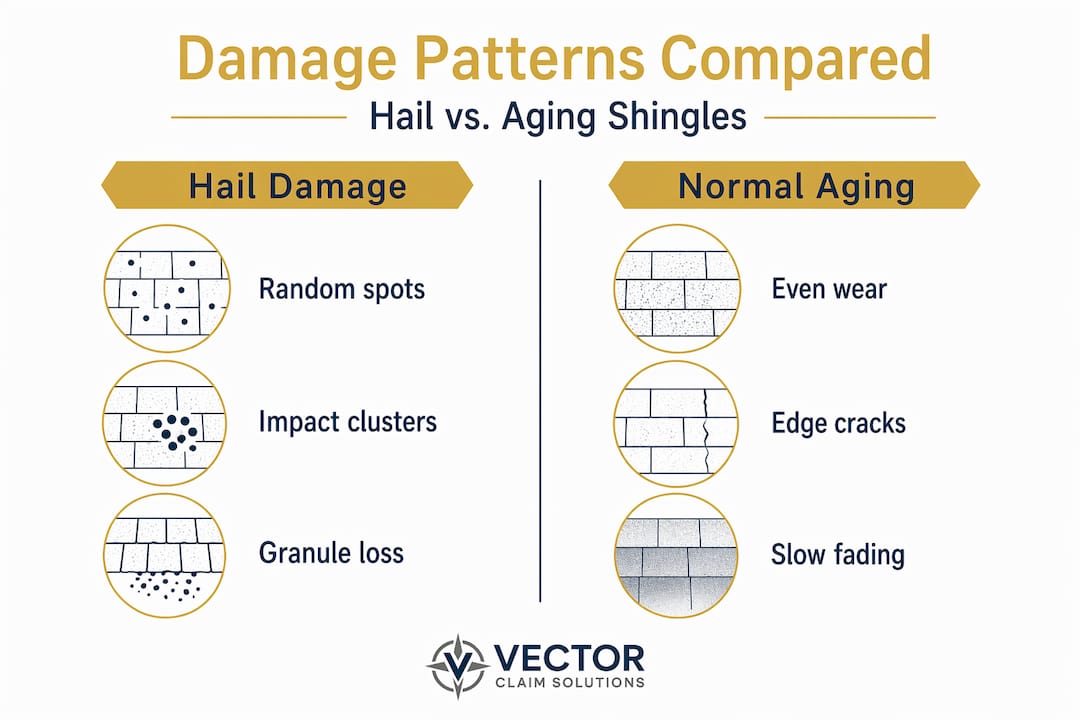

Hail damage vs. normal roof aging

One of the most common reasons hail claims get disputed is confusion between storm damage and ordinary wear. Knowing the difference protects you in conversations with your adjuster.

Hail damage has a distinct visual signature. Impacts cluster in patterns that correspond to the storm’s wind direction, and individual impact spots are circular or oval. Granule loss from hail creates bare patches surrounded by intact granules, rather than the gradual, uniform thinning you see from aging.

Normal aging, by contrast, produces even granule wear across entire slopes, consistent cracking along shingle edges, and gradual stiffening of the asphalt. It does not produce the random, scattered impact points that characterize hail.

| Feature | Hail damage | Normal aging |

|---|---|---|

| Granule loss pattern | Random, impact-centered spots | Even thinning across entire surface |

| Crack shape | Circular or impact-shaped | Linear, edge-following cracks |

| Distribution | Scattered, wind-direction aligned | Uniform across slope exposure |

| Soft metal evidence | Dents present on gutters, vents | No corresponding metal damage |

The 25% rule in roofing also matters here. When more than 25% of shingles are damaged or missing granules, full roof replacement is often recommended rather than spot repair. Understanding where your roof falls relative to that threshold shapes both your repair decision and your claim strategy.

You can learn more about spotting hail damage on your own roof with the detailed guide Vectorclaimsolutions has put together for homeowners.

My take on early detection after years in the field

I have reviewed hundreds of hail damage claims across Nebraska, Colorado, Texas, and Iowa, and the pattern I see most often is not fraud or exaggeration. It is homeowners who waited too long simply because their roof looked fine.

What I have learned is that the six-month window after a storm is genuinely critical. In my experience, claims filed within that window with solid photographic documentation and a professional inspection report are far more likely to result in fair settlements. Claims filed after a leak appears, without that early documentation, often turn into drawn-out disputes where the insurer attributes damage to aging rather than the storm.

The mistake I see homeowners make most often is assuming the inspection process will protect them. An insurance company’s adjuster is thorough, but their job is to assess damage within the bounds of what the carrier wants to pay. I have seen adjusters miss bruising, document fewer impact sites than actually exist, and categorize borderline damage as wear and tear. Getting an independent inspection is not about being adversarial. It is about having a complete, accurate picture.

What also surprises homeowners is how adjusters use meteorological data to reconstruct storm timelines. If your claim is disputed, that data can work for you or against you. Early inspection creates your own contemporaneous record that stands alongside that meteorological reconstruction, rather than leaving the insurer to tell the whole story.

The bottom line is simple: a $300 inspection right after a storm can prevent a $15,000 claim dispute six months later. Act early, document thoroughly, and do not assume your roof is fine just because it looks fine from your driveway.

— Vector

Get help protecting your hail damage claim

When hail damage progresses undetected, the financial stakes rise fast. Vectorclaimsolutions works directly with homeowners across Nebraska, Iowa, Colorado, Texas, and Florida to make sure damage is properly identified, documented, and presented to insurers the right way. We review existing estimates that may have missed damage, help you build a complete claim file, and negotiate with your carrier on your behalf. Understanding how insurance calculates claim payments is the first step toward knowing whether your settlement offer actually covers what your home needs. If you received an estimate after a recent storm and are not sure it reflects the full scope of damage, we can take a look.

FAQ

Why does hail damage get worse if left unrepaired?

Hail damage exposes roofing materials to UV rays, moisture, and temperature changes that cause further deterioration. Cracks widen through freeze-thaw cycles, and water eventually penetrates the damaged layers, causing rot and interior leaks months after the original storm.

How long after a hailstorm do roof leaks appear?

Interior leaks from hail damage can appear several months after a storm, because weakened shingles deteriorate gradually before water fully penetrates the roofing layers. This delay often makes it harder to connect the leak directly to the storm event.

Does hail damage affect my insurance claim if I wait to report it?

Yes. Evidence of hail damage fades within approximately six months as the exposed asphalt oxidizes, making it harder to prove the damage is recent and storm-related. Delayed claims face greater scrutiny and a higher risk of denial.

How can I tell the difference between hail damage and normal wear?

Hail damage creates random, circular impact spots with localized granule loss, often aligned with the storm’s wind direction. Normal aging produces even, gradual granule thinning across the whole slope without the scattered impact pattern or corresponding dents on gutters and vents.

When should I hire a public adjuster for hail damage?

Consider a public adjuster if your insurer’s estimate seems low, if your claim has been partially denied, or if your roof showed delayed symptoms that the carrier is attributing to age rather than storm damage. A public adjuster works on your behalf to document and negotiate the full scope of your loss.