When a major fire tears through your commercial building or a catastrophic storm leaves your property structurally compromised, the insurance claim that follows can feel just as overwhelming as the damage itself. Understanding the role of public adjuster large loss professionals play is one of the most practical steps you can take before, during, or after that process. The insurance company sends their own adjuster. That person works for the insurer. A public adjuster works exclusively for you, and in a large loss scenario, that distinction carries significant financial weight.

Table of Contents

- Key Takeaways

- The role of public adjuster large loss claims demand explained

- How public adjusters handle large loss claims step by step

- Unique challenges of large loss claims

- How public adjusters help maximize your settlement

- Practical guidance for hiring a public adjuster

- My take on public adjusters and large loss claims

- How Vectorclaimsolutions supports large loss policyholders

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Public adjusters work for you | They are licensed professionals hired by policyholders to represent their interests exclusively, not the insurer’s. |

| Documentation drives outcomes | Thorough scopes of loss, photos, and expert assessments directly increase settlement values in complex claims. |

| Large losses need specialized handling | Fires, major storms, and structural damage involve code upgrades and material matching disputes that require deep expertise. |

| Timing matters significantly | Missing proof-of-loss deadlines or appraisal demand windows can limit your claim options, even on valid claims. |

| Fees are tied to settlement results | Most public adjusters charge 5% to 20% of the final settlement, aligning their incentive directly with your recovery. |

The role of public adjuster large loss claims demand explained

Public adjusters are licensed professionals hired directly by policyholders to represent their interests in first-party property insurance claims. They do not work for the insurance company. They are compensated by you, the claimant, typically as a percentage of your final settlement amount.

That distinction matters more than most people realize. When you file a large loss claim, the insurer’s adjuster is assigned to evaluate damage and determine what the carrier owes. Their job is to represent the insurer’s position. A public adjuster’s job is the opposite: to build the strongest, most accurate claim possible on your behalf.

Core public adjuster responsibilities include:

- Policy review: Reading your policy in full to identify all applicable coverages, exclusions, endorsements, and limits relevant to your specific loss

- Damage documentation: Conducting a detailed site inspection with measurements, photographs, cause-of-loss narratives, and material inventories

- Scope and estimate preparation: Producing a complete repair estimate that reflects current material and labor costs, code upgrade requirements, and full replacement scope

- Claim submission: Organizing and submitting all documentation to the insurer in a structured, defensible format

- Negotiation: Representing your position through direct negotiation with the insurance company’s adjuster or legal team

- Supplement and reopen: Returning to pursue additional payment when an initial settlement does not cover the full cost of repair

On the fee side, typical public adjuster fees range from 5% to 20% of the claim settlement. Florida, for example, caps fees at 20% for standard claims and 10% during declared states of emergency under Florida Statute §626.854. Most states have similar licensing and fee cap frameworks, so verify what applies in your state before signing any contract.

How public adjusters handle large loss claims step by step

The process a public adjuster follows for large loss insurance claims is methodical. Here is what that workflow typically looks like from engagement to resolution:

-

Initial contract and scope discussion. You sign a representation agreement that defines the fee percentage, scope of services, and any applicable state-mandated terms. This is also when the adjuster reviews your policy to understand the full picture of your coverage.

-

In-depth policy analysis. Before touching the damage, a skilled public adjuster reads your policy carefully. They identify coverage triggers, exclusions that could be challenged, and endorsements that may apply to your specific type of loss.

-

Comprehensive site inspection. The public adjuster’s inspection goes far beyond a walkthrough. It includes detailed measurements, systematic photography, identification of secondary damage, cause-of-loss documentation, and a full material inventory. This is where large loss claims are often won or lost.

-

Scope of loss and repair estimate preparation. The adjuster builds a complete scope of loss that accounts for every damaged system, structure, and component. They use current pricing databases and, when needed, contractor input to produce estimates that reflect real-world repair costs.

-

Claim submission to the insurer. All documentation is submitted in a format that is clear, organized, and difficult to dispute. A well-structured claim submission reduces back-and-forth and positions you more strongly for negotiation.

-

Negotiation with the carrier. Your public adjuster meets, communicates, and negotiates directly with the insurance company’s adjuster. They counter low offers with documented evidence, not just verbal disagreement.

-

Supplements and reopened claims. When the insurer’s initial payment falls short, a public adjuster helps policyholders reopen claims or submit supplemental scopes. This is particularly common with hail and roof damage, where material matching and full replacement scope are frequently disputed.

-

Appraisal and dispute resolution. If negotiations stall, your adjuster can invoke the appraisal clause in your policy. Insurers can compel appraisal even during coverage disputes, though the appraisal process evaluates the amount of loss, not coverage questions. Understanding when appraisal helps versus when it is limited is part of the expertise a good public adjuster brings.

Pro Tip: Ask your public adjuster to walk you through your policy’s proof-of-loss deadline before they do anything else. Missing claims deadlines can restrict your options permanently, even when the damage is clearly covered.

Unique challenges of large loss claims

Large loss claims are not simply bigger versions of small claims. They carry a different category of complexity, and that complexity is where policyholders without representation tend to lose the most money.

Common disputes in large loss scenarios:

- Scope disagreements: The insurer’s adjuster may scope only visible damage while missing structural, mechanical, or water infiltration damage that a thorough inspection would reveal

- Code upgrade requirements: Local building codes often require upgrades when a structure is significantly damaged or rebuilt. Insurers frequently dispute or omit these costs. A public adjuster documents and fights for coverage of applicable code-required upgrades.

- Material matching: If half your roof, flooring, or siding is damaged, replacing only that portion may leave your property with mismatched materials. Large-loss structural events regularly involve disputes over whether matching materials or full replacement is warranted.

- Cause-of-loss disputes: Insurers may attribute damage to excluded causes. A well-documented cause-of-loss narrative from a public adjuster can counter this effectively.

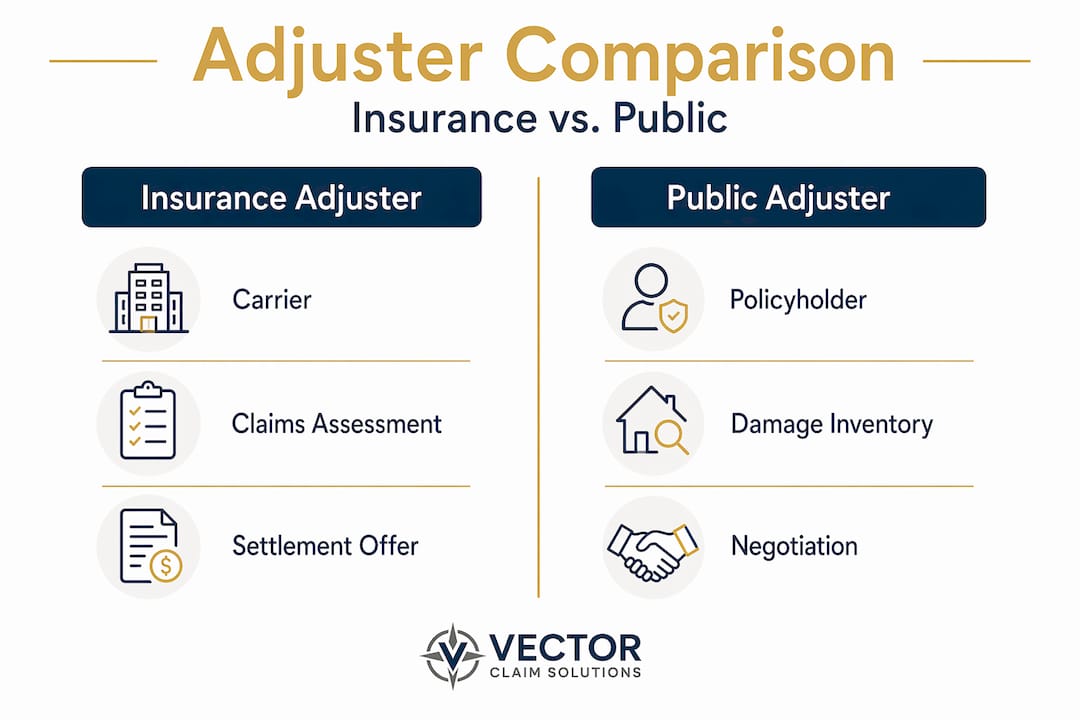

Public adjuster vs. adjuster: a direct comparison

| Factor | Insurance company adjuster | Public adjuster |

|---|---|---|

| Who they represent | The insurer | The policyholder |

| Who pays them | The insurance carrier | The claimant (% of settlement) |

| Claim scope focus | Minimize covered loss | Maximize documented loss |

| Availability | Assigned, not chosen | Selected by you |

| Negotiation role | Sets initial offer | Counters and negotiates for you |

Pro Tip: If your loss involves a fire, major storm, structural collapse, or any claim above $50,000, the complexity almost always justifies a public adjuster’s involvement. The fee pays for itself when a settlement doubles or triples from the initial carrier offer.

There are situations where a public adjuster adds less value. Simple claims with clear, undisputed damage and cooperative carriers may not need representation. But for anything that involves high repair costs, disputed causes, or multiple damaged systems, the expertise of public adjusters becomes a direct financial advantage.

How public adjusters help maximize your settlement

Settlement outcomes in large loss claims are not determined by who suffered the most damage. They are determined by who presents the most complete, accurate, and well-documented case.

Public adjusters protect policyholders against insurer tactics that aim to undervalue claims and push rushed settlements. Here is how they do it:

- Precise policy interpretation: Many policyholders accept a denial or low offer because they do not know their policy well enough to dispute it. Public adjusters identify coverage arguments the average policyholder would miss entirely.

- Thorough cost documentation: Documentation including detailed scopes of loss, photos, and expert assessments is the foundation of successful large loss negotiations. The difference between a $200,000 settlement and a $400,000 settlement is often entirely about what was documented and how.

- Expert witnesses and contractor input: On complex structural claims, public adjusters bring in engineers, contractors, or specialists whose professional assessments carry weight in negotiations and appraisal hearings.

- Preventing rushed settlements: Insurers sometimes push for quick resolution before the full scope of damage is known. A public adjuster holds that process open until every component of the loss is documented.

“The claim doesn’t get bigger because you suffered more. It gets bigger because you documented more.”

This is especially true for residential property damage claims where policyholders often accept the first number the carrier offers without understanding that it represents the insurer’s opening position, not their obligation.

Practical guidance for hiring a public adjuster

Knowing when and how to bring in a public adjuster is just as important as understanding what they do.

Signs you need a public adjuster include a settlement offer that seems far below your repair estimates, an insurer disputing the cause of loss, damage that was missed in the carrier’s initial inspection, or any loss event complex enough to involve multiple contractors and trades.

Here is a practical process for engaging one:

-

Check credentials first. Verify the adjuster holds a current license in your state. In Nebraska, Iowa, Colorado, Texas, and Florida, public adjusters are state-licensed professionals. An unlicensed person offering to “help with your claim” is a red flag.

-

Ask specific questions. How many large loss claims have they handled in your state? What is their fee structure? Can they provide references from clients with similar claim types? Do they have experience with your specific cause of loss, whether that is hail, fire, or water damage?

-

Review the contract carefully. Your agreement should clearly state the fee percentage, the scope of representation, any cancellation terms, and how supplements or reopened claims are handled. Some states require specific contract language by law.

-

Provide complete access. Your public adjuster needs full access to the property, your policy documents, prior claim history, and any communications you have already had with the insurer. Withholding information slows the process.

-

Stay engaged. You do not need to manage the claim yourself, but staying informed about key milestones, especially deadlines for proof-of-loss or appraisal demands, helps you protect your rights. Early engagement preserves claim options that can disappear if you wait.

Pro Tip: For commercial property losses, review our resource on hiring a public adjuster for commercial property. The contracting process and documentation requirements differ from residential claims in important ways.

My take on public adjusters and large loss claims

I’ve worked through enough large loss claims to know that most policyholders underestimate what they are dealing with when a significant event hits their property. They assume the process is straightforward: damage happens, insurer pays. What actually happens is far more layered.

The single biggest mistake I see is waiting. Policyholders spend weeks trying to negotiate on their own, accepting low offers, missing deadlines they did not know existed, and then calling for help when options have already narrowed. Timing in a large loss claim is not a minor detail. It shapes what you can recover.

What I’ve also learned is that documentation is not just paperwork. It is the argument. When an insurer’s adjuster issues a low scope, they are not necessarily acting in bad faith. They are writing what they can defend with the evidence in front of them. A public adjuster’s job is to change what is in front of them. When the claim file contains detailed measurements, expert cause-of-loss narratives, material specs, and code requirements, the conversation shifts. Carriers respond to what is documented, not to what you believe you deserve.

My honest view is that public adjusters are underused precisely because policyholders do not know they exist until they are already frustrated and behind. If you own property of significant value and you are in a storm-prone state, understanding this resource before you need it is a genuine advantage.

— Vector

How Vectorclaimsolutions supports large loss policyholders

At Vectorclaimsolutions, we work exclusively on behalf of property owners and businesses, not insurance carriers. We specialize in large loss claims across Nebraska, Iowa, Colorado, Texas, and Florida, covering storm damage, hail, wind, water, and major structural events.

If you have received an offer that does not reflect your actual repair costs, or if your claim has been denied or improperly scoped, we can help you understand what was missed and what your policy actually covers. Start by reviewing how public adjuster documents are structured to understand the documentation standard that drives better outcomes. For a direct review of your current claim, visit Vector Claim Solutions and request a no-pressure second opinion on your settlement.

FAQ

What does a public adjuster do in a large loss claim?

A public adjuster reviews your policy, inspects and documents all damage, prepares a full repair estimate, and negotiates with your insurer to maximize your settlement. They represent you exclusively, not the insurance company.

How is a public adjuster different from an insurance adjuster?

An insurance company adjuster represents the carrier and evaluates claims on the insurer’s behalf. A public adjuster is hired by and paid by the policyholder, working solely to protect the policyholder’s financial recovery.

When should I hire a public adjuster for a large loss?

Hire a public adjuster when your damage is complex, your settlement offer seems low, your claim involves disputes over cause or scope, or when your loss exceeds $50,000. Early identification and hiring helps avoid delays and preserve claim options.

What does a public adjuster typically charge?

Typical fees range from 5% to 20% of the final claim settlement, depending on your state and claim complexity. Some states cap fees during declared emergencies.

Can a public adjuster reopen a claim that has already been settled?

Yes, in many cases. If new damage is discovered or the initial scope was incomplete, a public adjuster can submit a supplemental claim or request the claim be reopened, particularly for hail, roof, and water damage losses where full scope is commonly disputed.