When property damage forces you into an insurance claim, the process rarely feels straightforward. You are suddenly expected to understand policy language, coordinate inspections, and get fair compensation, all while managing the stress of a damaged home or building. Knowing how to work with a public adjuster contractor setup correctly, keeping each professional in their defined role, is the single biggest factor separating underpaid claims from fully settled ones. This guide gives you a practical, step-by-step framework for collaborating with both professionals so your claim gets handled right the first time.

Table of Contents

- Key takeaways

- How to work with a public adjuster contractor effectively

- Before you engage either professional

- Step-by-step: collaborating through your claim

- Pitfalls and legal considerations to know

- Verifying your settlement and repair alignment

- My take on what actually makes or breaks these claims

- How Vectorclaimsolutions supports your claim from start to finish

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Roles must stay separate | Public adjusters handle claim negotiation; contractors handle damage documentation and repairs. |

| Verify credentials first | Confirm your public adjuster’s license and your contractor’s registration before signing anything. |

| Documentation drives outcomes | Contractor-produced damage records aligned with insurer categories give public adjusters the strongest foundation. |

| Communication channels matter | Keep claim negotiations with your public adjuster; communicate repair logistics directly with your contractor. |

| Watch for legal red flags | Contractors who offer to handle your claim negotiation may violate state licensing laws. |

How to work with a public adjuster contractor effectively

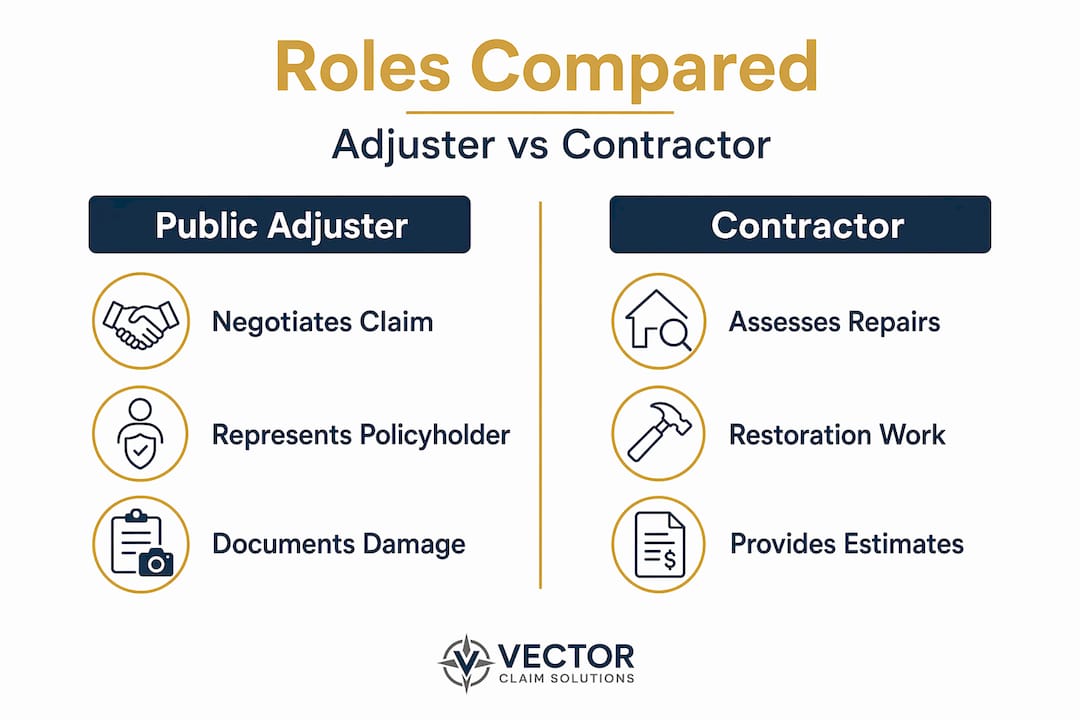

The biggest homeowner mistake is assuming public adjusters and contractors perform the same function. They do not, and blurring that line is where most claims go wrong.

A public adjuster is a licensed professional who represents you, the policyholder, when negotiating with your insurance carrier. Their job is to review your policy, document covered losses, prepare your claim package, and negotiate the settlement amount on your behalf. They do not swing hammers or order materials. Their entire focus is the claim.

A contractor assesses physical damage, provides repair estimates, and performs the actual restoration work. Their expertise is construction, not insurance law. They know what is broken and what it costs to fix it. They are not equipped to interpret policy language or negotiate with adjusters.

Here is a side-by-side breakdown of how these roles divide:

| Function | Public Adjuster | Contractor |

|---|---|---|

| Represents policyholder | Yes | No |

| Negotiates with insurer | Yes | No (prohibited in many states) |

| Documents repair scope | Supports and organizes | Primary responsibility |

| Performs repairs | No | Yes |

| Paid by | % of settlement | Repair contract |

| Licensed by | State insurance board | State contractor board |

Public adjusters typically charge between 10% and 20% of the final settlement amount, with state-specific fee caps. Contractors are paid directly from settlement funds under a separate repair agreement. These are two distinct financial relationships, and they should always be documented separately.

Before you engage either professional

Getting organized before you hire anyone will save you significant time and protect you from avoidable problems. Here is what to do before signing any contract.

- Verify public adjuster licensing. Each state maintains a searchable license database. In Nebraska, Iowa, Colorado, Texas, and Florida, public adjusters must hold an active state-issued license. Do not accept verbal assurances. Look them up directly.

- Check contractor registration and insurance. A legitimate contractor carries general liability insurance and, where required, a state contractor’s license. Always request certificates before allowing inspection access.

- Confirm fee percentages in writing. Your public adjuster’s fee should be clearly stated in a written engagement agreement. State regulations require verification of separate licensing and caution against combined negotiation and repair roles.

- Use separate contracts for each professional. One agreement with your public adjuster, one with your contractor. Never sign a combined document that attempts to cover both roles.

- Clarify the contractor’s boundaries up front. Make clear that your contractor will document damage and perform repairs but will not communicate with the insurance carrier or negotiate on your behalf.

Pro Tip: Ask your public adjuster directly whether they have worked alongside contractors in your region. A public adjuster familiar with Nebraska hail claims or Florida wind events will understand the local damage patterns that carriers often dispute.

If you are unsure whether your situation warrants a public adjuster, this resource on signs you need a public adjuster after a storm offers a clear set of indicators.

Step-by-step: collaborating through your claim

This is where preparation turns into results. The following process reflects how successful claims typically move when public adjusters and contractors work together without crossing roles.

-

Start with an independent contractor inspection. Before the insurance adjuster visits, have your contractor conduct a thorough inspection of all damaged areas. Photograph everything. Note dimensions, materials, and areas of suspected hidden damage. Roof damage documentation is particularly important here, since adjusters can miss less-visible damage without expert documentation from a construction professional on site.

-

Have the contractor present at the insurance adjuster’s inspection. This step alone can significantly change the claim outcome. The contractor can walk the insurance adjuster through each damaged component, point out areas that are easy to overlook, and challenge on-the-spot scope decisions with documented evidence. Their presence signals that you are organized and prepared.

-

Give contractor documentation directly to your public adjuster. The highest leverage collaboration occurs when contractors document damage aligned with insurer categories. This allows your public adjuster to build a claim package without redundant work. If the contractor’s notes are organized by damage type and location, your public adjuster can move faster and build a stronger file.

-

Let your public adjuster lead all claim communication. Once documentation is in their hands, the public adjuster handles the insurer. They respond to carrier requests, push back on scope reductions, and negotiate the settlement. You should not be relaying messages through your contractor. Homeowners who communicate primarily through contractors risk ethical and regulatory problems that can slow or complicate a claim.

-

Handle repair logistics separately with your contractor. While the claim is being negotiated, you can discuss timeline, materials, and repair phasing directly with your contractor. Keep these conversations entirely separate from claim negotiations.

-

Make final decisions yourself. Both professionals advise you. Neither one authorizes action on your behalf without your consent. You sign off on repair contracts and settlement agreements.

Pro Tip: Ask your public adjuster to provide a written summary of what the settlement covers before you authorize any repair work. Comparing that summary against the contractor’s repair estimate is the fastest way to catch scope gaps before work begins.

Pitfalls and legal considerations to know

Not every contractor or public adjuster operates with your best interest in mind. Understanding the most common problems will help you avoid costly mistakes.

- Contractors acting as claim negotiators. Contractors should not prepare claims, negotiate with insurers, or act as claim advocates. These actions may violate consumer protection and insurance laws. In Texas specifically, a roofing contractor cannot act as a public adjuster on the same claim due to separate licensing requirements and conflict of interest laws.

- Assignment of benefits (AOB) clauses. Some repair contracts include AOB language that transfers your right to claim payments directly to the contractor. Once signed, you lose significant control over how settlement funds are used. Read every contract before signing and ask your public adjuster to review it.

- Combined negotiation and repair companies. Conflicts arise when companies try to cover both repair and claim negotiation roles. This creates a financial incentive that may not align with your best outcome.

- Pressure to sign quickly after a storm. Contractors who appear at your door within hours of a weather event and push for immediate signatures are a warning sign. Legitimate professionals give you time to review agreements.

- Unlicensed public adjusters. Anyone offering public adjuster services without a current state license is operating illegally. Consumer protection guidance in Iowa and other states frames public adjusters as negotiation experts distinct from contractors, emphasizing the need for homeowners to verify credentials independently.

“Maintaining clear separation of duties protects homeowners from regulatory violations and claim disputes. If someone is offering to both fix your roof and settle your claim under one contract, ask why.”

For additional legal context on protecting yourself during major property claims, this overview from Oaks Law Firm on what to do after a property disaster addresses several relevant legal boundaries.

Verifying your settlement and repair alignment

Once your public adjuster reaches a settlement with the carrier, your job is not done. You need to confirm that what was negotiated actually covers what needs to be repaired, and that the contractor delivers accordingly.

Start by reviewing the settlement documents line by line with your public adjuster. The claim scope should specify each damage category, the repair method, materials, and dollar allocation. If anything is unclear, ask for clarification before accepting.

Then compare the contractor’s repair estimate against the approved scope. Gaps are common. Insurance carriers sometimes approve a narrower scope than what is physically necessary, and contractors sometimes estimate costs higher than the settlement covers.

| Check | What to look for |

|---|---|

| Settlement vs. estimate | Do approved dollar amounts cover contractor repair costs? |

| Scope completeness | Are all documented damage items included in the settlement? |

| Material specifications | Do insurer-approved materials match what the contractor recommends? |

| Supplement triggers | Has any damage been overlooked that warrants a supplement claim? |

When discrepancies appear, communicate them to your public adjuster immediately. Supplement claims, which request additional payment for items missed in the original settlement, are a normal part of the process. Your public adjuster can file supplements as long as the claim remains open, so do not wait or assume the gap cannot be addressed.

Use roof damage documentation best practices to ensure you have the evidence needed to support any supplement requests. Thorough records from the initial inspection give your public adjuster the material they need to push back effectively.

My take on what actually makes or breaks these claims

I have seen more claims than I can count fall apart not because of bad documentation or low settlements, but because of blurred communication. Someone assumes the contractor is keeping the public adjuster informed. The contractor assumes the homeowner approved a scope change. The public adjuster is working from outdated information. By the time anyone realizes what happened, the claim is underpaid and everyone is pointing at someone else.

What actually works is deliberate separation. The contractor stays in their lane. The public adjuster stays in theirs. And you, as the property owner, stay engaged with both. That does not mean micromanaging. It means attending inspections, reviewing summaries, and asking questions when something does not match.

The second thing I have learned is that documentation quality at the contractor level determines everything downstream. When a contractor’s inspection report is organized, specific, and categorized by damage type, a public adjuster can build a claim package in hours instead of days. Poor contractor documentation means the public adjuster essentially starts over. That delays your settlement and creates more room for the carrier to push back.

My honest advice: before you hire anyone, ask both professionals how they have worked together in the past. If a public adjuster cannot name contractors they trust, or if a contractor cannot describe how they support a public adjuster’s documentation process, that is information worth having before you commit.

— Vector

How Vectorclaimsolutions supports your claim from start to finish

When you work with a public adjuster contractor team that understands how to stay in their respective lanes, the results are measurably better. At Vectorclaimsolutions, we work with residential and commercial property owners across Nebraska, Iowa, Colorado, Texas, and Florida to do exactly that.

We specialize in identifying underpaid, denied, and improperly scoped claims and correcting them through construction-level damage analysis and structured carrier negotiation. We know how to collaborate with contractors to extract the documentation that actually moves a claim forward. Our approach is explained in detail in how adjuster documents are structured, which gives you a clear picture of what strong claim documentation looks like.

If your current estimate feels too low, or if you are not sure your contractor and adjuster are working from the same playbook, we offer a no-pressure claim review to assess where things stand. Use our claim checklist as a starting point.

FAQ

What does a public adjuster actually do?

A public adjuster represents the policyholder, not the insurance company, during the claims process. They document damage, interpret policy coverage, and negotiate the settlement amount directly with the carrier.

Can my contractor negotiate my insurance claim?

In most states, contractors cannot negotiate claims or act as claim advocates, as these actions may violate consumer protection and insurance laws. Hire a licensed public adjuster for that role.

How much does a public adjuster cost?

Public adjusters typically charge 10% to 20% of the final settlement amount, depending on the state and claim complexity. Always confirm the fee percentage and any state-mandated caps in a written contract before engagement.

Should my contractor attend the insurance inspection?

Yes. Having a contractor present during the insurance adjuster’s inspection is strongly recommended, as adjusters can miss less-visible damage without construction expertise on site to highlight it.

What is an assignment of benefits clause?

An assignment of benefits (AOB) clause in a repair contract transfers your right to claim payments directly to the contractor. Read all repair contracts carefully before signing and have your public adjuster review any AOB language to protect your interests.